US markets fell for the shortened week after a 2-week upstreak as good news spelt bad news, that a strong US economy will prompt the Fed to keep rates higher for longer. Bond traders have been ratcheting up bets that the Federal Reserve isn’t done with its interest-rate hikes just yet. With the economy defying gloomy forecasts and energy prices rising, economists are forecasting the biggest monthly jump in 14 months — and the swaps market is pricing in risk that it will come in even higher than expected. Brent oil climbed above $90 a barrel – a 9-month high and was on track for a small weekly gain after supply curbs from OPEC+ leaders Saudi Arabia and Russia were extended for the rest of the year. Growing tensions between US and China added to the risk off sentiment with China banning the use of Apple’s i-phones in government and state owned businesses and the US probing a made in China chip housed within Huawei’s latest smartphone.

Applications for US unemployment benefits fell to the lowest since February fanning speculation the Fed could turn hawkish again after pausing later this month. Another data point supporting this narrative was the services industry, which expanded more than expected in August. On the positive side, signs of a cooling labor market stoked optimism that the Fed may be done, with futures traders seeing a roughly 50% chance that it will raise rates one more time in November after holding steady at the Sept. 19-20 meeting.

Apart from CPI on Wednesday, we will have retail sales, industrial production and PPI to cap the week’s releases. Headline CPI YoY is expected to accelerate to 3.6% from 3.2% whilst the monthly core CPI is expected to come in unchanged at 0.2%. No Fedspeak this week as the blackout period starts for the next FOMC meet.

In investments, we recommend floaters and shorter duration (BBB+ ~ 5.5% yield, duration 2.6 years) over longer duration for the moment, as long dated yields continue to hold up. Resilient data and talks of growth sustainability and new issues add to LTyield volatility.

China and Hong Kong started the week strong up 1.4% for Shenzen and up 2.5% for HangSeng index on Monday. In Hong Kong, the mainland property index surged by 8% on the back of the slew of property sector related support announced. But the rally was short lived.

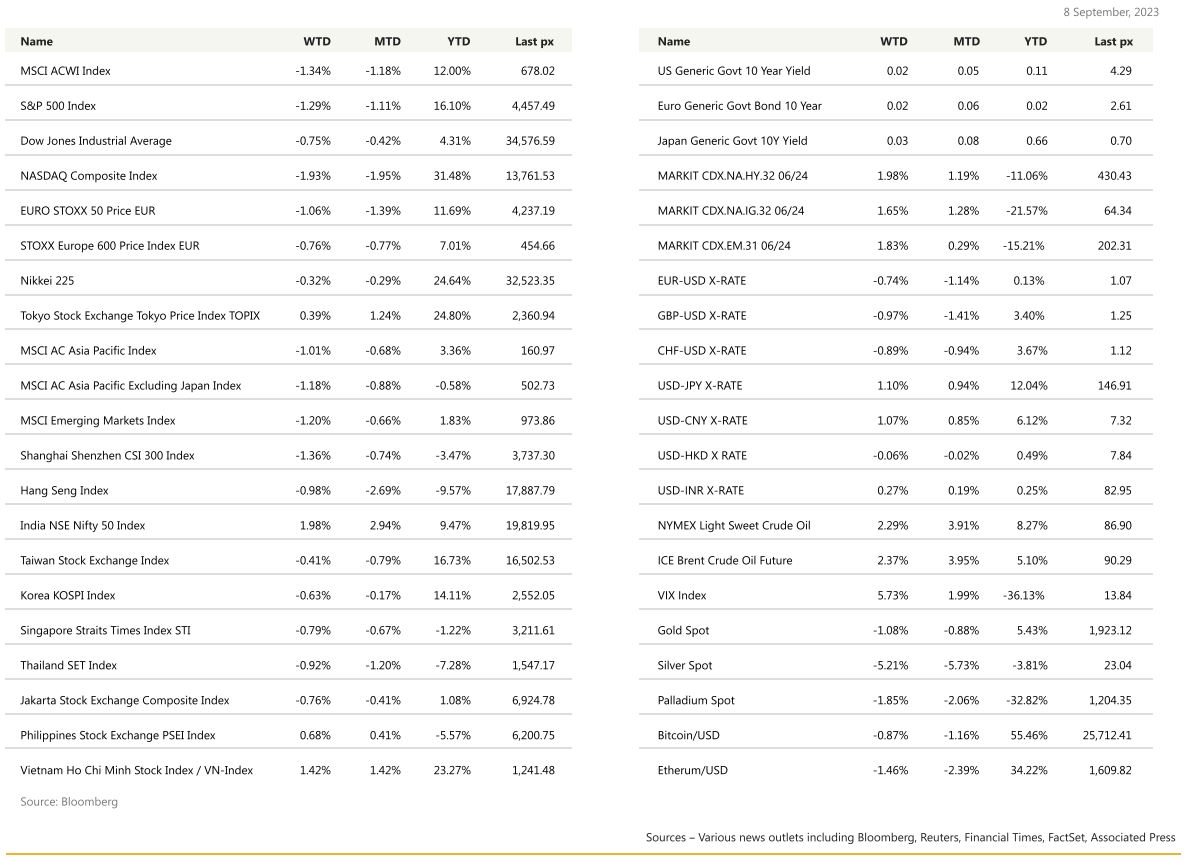

Asian equities ended lower last week. More losses for the Hang Seng, which is now in the red for the week despite the property sector rally we saw at the start of the week; mainland stocks also lower. (CSI -1.36%, HSI -0.98%) Japan too was lower (NKY -0.32%), Australia dragged down by commodity stocks post China’s trade data (ASX 300 -1.7%). India broke to four-week highs to close +1.98%. Vietnam and Philippines were the other benchmarks to show a gain, up 1.42% and 0.68% respectively for the week.

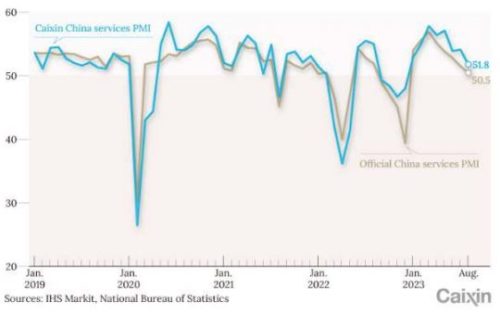

Some data points out of Asia in the last week – Caixin China General Services Business Activity Index, which provides an independent snapshot of operating conditions in services industries such as retail and travel, dropped to 51.8, the lowest this year in China.

Japan household spending shrunk by most in 2.5 years amid sharp fall in housing category.

India PMI dipped a little but still at expansive 60.9. Singapore’s retail sales growth increased slightly from last month’s two-year low.

Expansion in China’s Services Activity Weakens

Headline inflation in Emerging Asia appear to be rising again as higher food and energy costs push August CPI readings higher to give regional central banks fresh headaches amid slowing economic growth.

Taiwan latest to post seven-month high y/y headline inflation of 2.3% from July’s 1.9%, above central bank target range.

Follows higher headline inflation readings in Indonesia (3.3% from 3.1% y/y), Philippines (5.3% from 4.7%), South Korea (3.4% from 2.3%), Thailand (0.9% from 0.4%), Vietnam (3.0% from 2.1%). Core inflation remains on downward trajectory in all these countries giving central banks, governments time to address headline inflation with fiscal measures, economists say.

Japan’s core inflation is following the path of G10 peers, and if that persists, it could soon be a lot higher than the BoJ forecasts. G10 central banks have also tended to start hiking when core inflation was 2%pt above their target, where Japan is now. The RBA kept policy on hold as expected in September and retained its hawkish bias. DB still expects two more 25bp hikes in November and December this year. Data will need to rebound from the soft tone of the past month to justify those hikes, but already there is evidence that could happen as early as the next monthly CPI print.

Thailand is likely to ease visa rules for Chinese and Indian travellers and allow longer stays for visitors from all nations as new Prime Minister Srettha Thavisin looks for ways to boost tourism revenue to nearly $100 billion next year. The new stimulus measures are likely to be announced after the first cabinet meeting which is to take place in early-Sep 23.

- We expect AOT (airport), ERW (hotels) , SPA (wellness centres) and CENTEL (hotel) to benefit the most from the potential visa exemption for Chinese tourists.