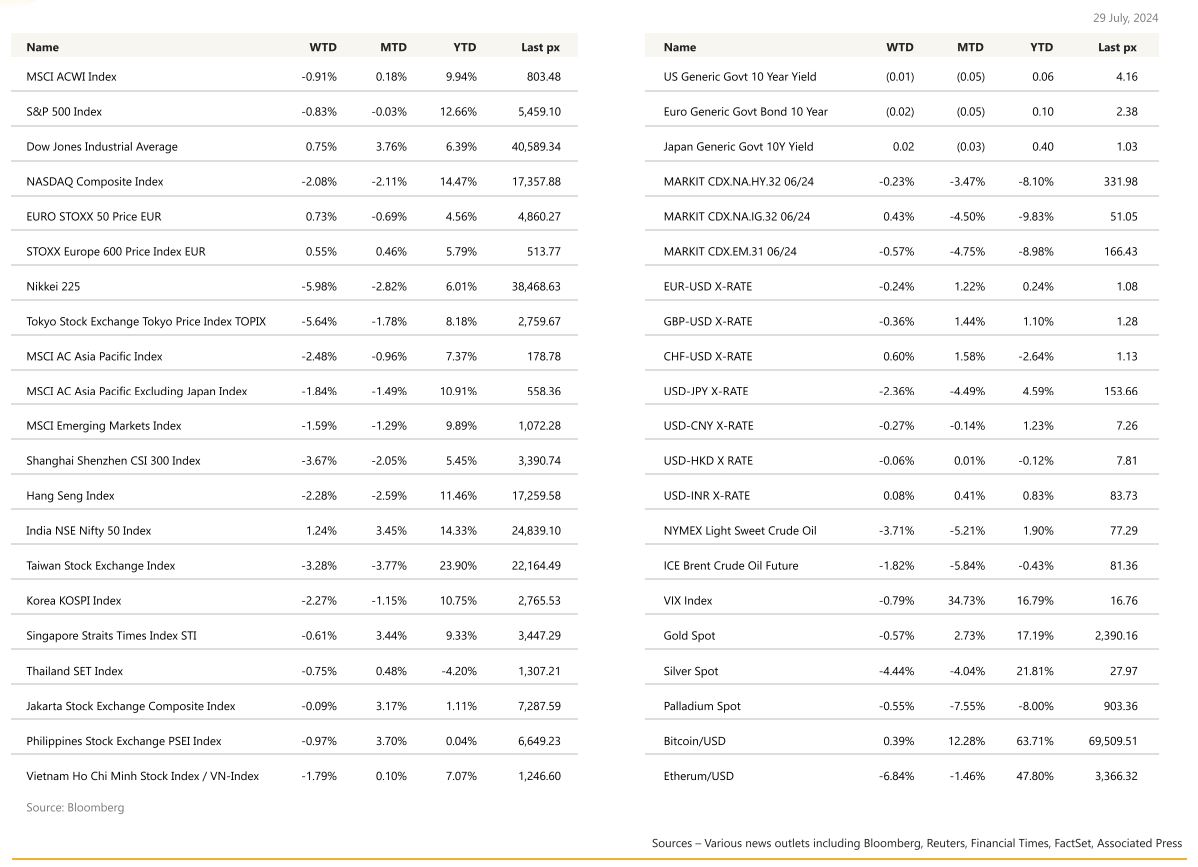

KEY MARKET MOVES

MACRO OVERVIEW

US

It was the story of the “great rotation” all week, culminating from a shift out of BIG Tech and into the smaller to mid-cap cyclical sector, which saw the Nasdaq lose just on 2% and the Russell 2000 Index powering to a 3.5% close. The selloff in Tech took a pause on Friday on optimism that the Fed Reserve may be able to cut interest rates sooner rather than later. $2.6 trl was erased from the market value of firms in the tech-heavy gauge since it hit a record on July the 10th. The correction was largely seen as healthy as risk remained vested and market breadth improved with more than 400 companies in the S&P 500 advancing while roughly 15% fell. Friday’s rally came after the Fed’s preferred inflation gauge — the so-called core personal consumption expenditures price index — showed price pressures are contained, bolstering speculation that it will start easing monetary policy by September. Core PCE MoM came in at 0.2% as expected, and YoY at 2.6% vs expectation of 2.5%. Headline PCE YoY came in at 2.5% from 2.6% previously. The PCE data is one of the last inflation indicators before the Fed meets this week on July the 31st. Other data out earlier was personal spending which continued to hold up, and an annualised GDP QoQ of 2.8% after rising 1.4% in the previous period, beating expectations. The narrative of a soft landing that the Fed is engineering appears to be holding true. Apart from the rotation story, earnings from Tesla and Alphabet underwhelmed, contributing to the switch. The flight to quality that we’ve seen all year long, is becoming vulnerable to earnings that cannot have even minor disappointments. Still, the theme is not dead with Microsoft Corp. betting that artificially intelligent assistants will transform workplaces around the world, generating new excitement and revenue for a very old product like the Office productivity software used by hundreds of millions of workers. The U. of Mich. Inflation expectations for 1 Yr and 5-10 Yrs came in at 2.9% and 3.0% respectively, largely in line with expectations. In politics, Biden stepped down and VP Kamala Harris has been endorsed to take on Trump. Her running mate is yet.

Cryptos fared well for the week, with an upgrade from Citi on Coinbase from neutral to buy as analysts said the regulatory risk-reward balance for the crypto exchange is improving given the changes in the upcoming US election dynamics (Trump favours cryptos!). BTC flirts with $68k whilst ETH lagged behind at $3,300.

This week will start with the JOLTS openings on Tuesday, followed by the ADP employment data on Wednesday, FOMC decision early Thursday morning and on Friday, the all-important NFP unemployment release – 178k jobs expected to be created at an unchanged unemployment rate of 4.1%.

We like the Trump-themed trades of utilities (electric companies) and financial services where over-regulation could be eased further, in spite of lower rates.

Europe

The European stock 600 index closed 0.9% higher London time with nearly all the sectors across the region trading in positive territory. Construction and material and household goods led gains, up 1.8% and 1.7% respectively. Travel and leisure stocks were also 1.6% higher. Last week, a lot of data on business confidence in July was published. However, they pointed down and did not support an acceleration of activity at the start of 3Q. The composite euro area PMI shed 0.8 pts to 50.1. Most of the fall was in services: -0.9 pts to 51.9. Manufacturing was more resilient but is already much lower: -0.2 pts to 45.6. By country, the German composite PMI fell 1.7 pts to 48.7, while the French composite, apparently buoyed by the Olympic Games, increased 1.3 pts to 49.5.

In a Europa Press Interview published last week on 23 July, Guindos, the Vice President of the ECB emphasized the importance of the September macroeconomics projections in determining the September rate decision. Overall, for a September rate cut to happen, the ECB Governing Council will want to see the September projections unchanged or improved relative to June. In addition, the Q2 2024 negotiated wage growth slowing and lastly the underlying momentum in services inflation moderating.

On Tuesday 30 July, flash estimates for 2Q GDP will be released and the July Consumer Confidence. Inflation in July will then follow, with the Spanish and German flash estimates on Tuesday 30 July and French, Italian and euro area figures on Wednesday 31 July. Labour market data will be another highlight, with German unemployment out on Wednesday 31 July and euro area unemployment on Thursday 1 August.

In the UK, this Thursday would be the BoE August meeting and the only data point that may have been able to unsettle the BoE was the flash PMIs. The spike in services PMI employment to 52.7 in July from 50.5 in June showed strong labour market activity and it was the highest index since June 2023. This fed into concerns about excessive labour market strength. The manufacturing PMI input prices indicator rose to 57.9 in July and this is in strong expansionary territory but it is only the second consecutive month of increase. It might be due to the reflection of higher shipping prices. The CBI industrial trend looked dovish across the major categories, with total orders, selling prices and business optimism falling sharply.

As for the BoE’s August meeting, markets are pricing an equal probability of a hold and a cut. Over the past year, market pricing an August cut has been very volatile. At the start of 2024, markets were expecting to have already been a 100bps of cuts after the August meeting.

Asia

Hong Kong stocks ended lower as the PBOC surprised by cutting a key interest rate. Hang Seng -2.28% for the week while, CSI 300 Composite down 3.67%. Nikkei was lower by 5.98% last week, weighed by double-punch of a technology selloff and stronger yen rallied to its highest against the dollar since May and is also notably stronger against other major currencies. The rest of North Asia also closed weaker from the tech rout. Taiwan was lower by 3.28% and South Korea lower by 2.27%. Indian benchmarks were up, closing higher by 1.24% last week.

India Budget highlights : India’s Modi Government has set aside billions for jobs, allies in post-election budget. The $576 billion in total outlays included $32 billion for rural programs $24 billion to be spent over five years to create jobs, and more than $5 billion for two states ruled by coalition partners. Despite the new spending, India cut its fiscal deficit target to 4.9% of gross domestic product in fiscal year ending on March 31, 2025, from 5.1% in February’s interim budget, helped by a large surplus of $25 billion from the central bank. The government also marginally reduced gross market borrowing to 14.01 trillion rupees.

- India raised to 20% from 15% its tax rate for equity investments held for less than a year, while the rate for those held longer than 12 months rose to 12.5% from 10%. The taxes will be applicable from Wednesday (24 July) .

- Corporate tax for foreign companies was cut to 35% from 40%, with the aim of encouraging more investment, while a lower tax burden for lower income consumers, expected to encourage spending, helped drive consumer stocks to record highs.

- Customs duty on gold and silver reduced to 6 per cent and platinum to 6.4 per cent.

- New 109 high-yielding and climate-resilient varieties of 32 field and cultivation crops to be released for farmers. In the next 2 years, 1 crore farmers will be initiated into natural farming. 10,000 need-based bio-input resource centres will be established.

- Mobiles to get cheaper: Duty reduced to 15% on mobile phone / Custom duty hiked on plastic products

- The Indian rupee slipped to record lows as raising tax rates for capital gains from equity investments and on equity derivative trades hurt market sentiment.

Taiwan’s export orders rose less than expected in June on weak demand from the island’s top trading partner China and for laptops and mobile phones, even as chips saw continued strength from a boom in artificial intelligence (AI) applications. The ministry said it expects export orders in July will come in between a contraction of 2.6% and expansion of 1.6% year-on-year. Orders from Europe picked up in June, growing 6.3%, after being flat in May. Taiwan’s orders from Japan, orders slid 9.2% last month, versus a contraction of 15.1% in May.

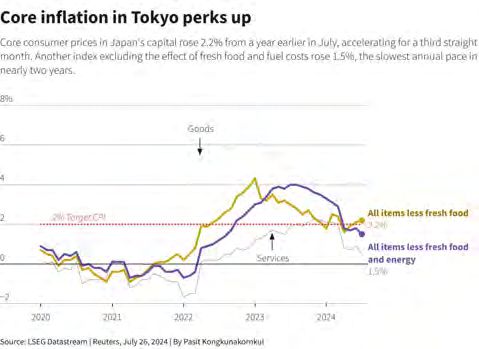

Japan manufacturing purchasing managers’ index (PMI) slipped to 49.2 in July from 50.0 in June. Service providers led the expansion. Services PMI rose to 53.9 in July, the highest in three months, while manufacturers saw a renewed reduction in output that was only marginal. Manufacturers remained pressured as input cost inflation intensified to the highest level since April 2023, while output prices eased to a four-month low, it found. Core inflation in Japan’s capital accelerated for a third straight month in July but an index gauging demand-driven price growth slowed, data showed on Friday.

South Korea’s economy unexpectedly shrank in the second quarter, clocking the sharpest contraction since 2022. GDP for the April-June period fell 0.2% from a quarter earlier in seasonally adjusted terms, data from the Bank of Korea showed, missing a 0.1% gain expected by analysts. The weak data, along with easing consumer price pressures seen in June, increases calls for the BOK to cut interest rates as soon as next month, some analysts say.

FSSTI in Singapore was lower by 1.44% last week, taking YTD gains to 9.35%. Singapore’s core inflation in June dropped to 2.9% year-on-year – the lowest in more than two years. The decrease was driven by lower inflation for retail and other goods, as well as services. And, last Friday, the Monetary Authority of Singapore (MAS) as it kept its monetary policy unchanged. It said core inflation – which excludes accommodation and private transport – is expected to “step down more discernibly” in the fourth quarter of this year and into 2025.

This week we have major central banks meeting. Monetary policy decisions in Japan, the US and the UK are in focus after global markets were ravaged last week by a rally in the yen on bets the Bank of Japan may hike its key rate.

GeoPolitics

US- Japan : Japan will continue to work with the United States for peace on the Taiwan Strait regardless of who is in the White House after the November presidential election, Japan’s top government spokesperson told Reuters in an exclusive interview. The comments come after Republican presidential candidate Donald Trump said Taiwan should pay the U.S. for its defence, raising concerns over American support for the island nation should the former president be re-elected.

Palestine – China : Palestinian rivals including Hamas and Fatah agreed to form a unity government at talks hosted by China, Beijing said on Tuesday, a deal meant to deliver a post-war Gaza administration but quickly rejected by Israel. The meeting was held amid attempts by mediators to reach a ceasefire deal after nine months of war between Israel and Hamas inGaza. One of the sticking points is the “day-after” plan – how the Hamas-run enclave will be governed once the war, which began on Oct. 7, ends.

China – Nvidia is working on a version of its AI chip for the China market that would be compatible with US export controls. It said Nvidia will work with one of its major distribution partners, Inspur, on the launch of the chip following trade sanctions that were imposed in 2023.

Credit / Treasuries

US Treasury yield curve twist steepened last week, with the 2 years falling 12.77 bps, 10 years down 4.5 bps and 30 years rising 0.55 bps. Market continued to price the first Fed cut to be in September and at least 2 cuts this year, as US core PCE deflator came in in-line with consensus. On the credit side, spreads in the US IG and HY closed the week relatively unchanged, with the IG at 51.048 and HY at 106.748 bps.

FX

DXY USD Index fell 0.08% to close the week at 104.32, driven by USDJPY weakness, despite USD rising against EUR/GBP/CHF. Risk off due to fading enthusiasm about the AI frenzy supported USD. Data wise, advance reading for Q2 GDP showed economy growing at 2.8% qoq , well ahead of consensus 1.9% and prior quarter’s final 1.4%. Core PCE Price Index mom came in in-line at 0.2%, driving the yoy to 2.6%, slightly above consensus at 2.5%. Michigan consumer sentiment came in at 66.4 (C: 66.5, P: 66.0).

EURUSD fell 0.24% to close the week at 1.0856. Data wise, EU Composite PMI for July preliminary came in at 50.1 (C: 50.9), with both manufacturing and services PMI below consensus. ECB 1 year and 3 years CPI expectations remain the same as prior months. Immediate support at 1.0821 (200 DMA) and 1.08 (100 DMA).

GBPUSD fell 0.36% to close the week at 1.2867. Data wise, UK Composite PMI for July Preliminary came in at 52.7 (C: 52.6, P: 52.3), with manufacturing above consensus and services slightly below consensus. Immediate support at 1.2781 (50 DMA) and 1.2683 (100 DMA). Resistance level at 1.3044 (YTD high).

USDJPY fell 2.36% to close the week at 153.76, at one point touching 152 (intraweek low), as carry trade in JPY was unwound, reflecting wagers that the interest rate gap between Japan and US will likely narrow. Media report that BoJ is likely to debate on rate hike this Wednesday and unveil a plan to roughly halve bond purchases. Swap market now pricing a roughly 70% chance of a BoJ rate hike next week, up from 44% from two weeks ago. Data wise, Japan Tokyo CPI came in at 2.2% yoy (C: 2.3%). Core CPI was in-line at 2.2% yoy, while Core-Core CPI came in below consensus at 1.5% (C: 1.6%, P: 1.8%).

Oil & commodities

Oil future fell last week, with WTI down 3.71% to 77.16 and Brent down 1.82% to 81.13, on declining China demand and hopes of a Gaza ceasefire agreement that could ease Middle East tensions and accompanying supply concerns. This was despite DOE reports that crude and gasoline stockpiles fell more than expected. U.S. crude oil inventories have depleted faster than normal over the last four weeks – keeping spot prices firm and the futures curve in a steep backwardation. Support level on Brent at 80 and WTI at 75.

Gold fell 0.57% to close the week at 2,387.19 due to USD strength from risk off sentiment, at one point trading at 2,353.24 (intra-week low). In addition, higher than consensus US Q2 GDP supported higher for longer narrative.

Economic News This Week

-

Monday – SW Retail Sales, UK Mortg. App., US Dallas Fed Mfg Act.

-

Tuesday – JP Jobless Rate, AU Building App., EU Cons./Svc/Indust./Econ. Confid. / GDP, US Cons. Confid.

-

Wednesday – NZ Building Permits, JP Retail Sales/ Indust. Pdtn/ BoJ Rate Decision, CH PMI, AU Retail Sales/ CPI, EU CPI, US MNI Chic. PMI/ FOMC Rate Decision

-

Thursday – AU/JP/CH/EU/UK/CA/US Mfg PMI Jul Final, AU Trade Balance, UK Hse Px, EU Unemploy. Rate, UK BOE Rate Decision, US Initial Jobless Claims/ ISM Mfg/ ISM Prices Paid

-

Friday – JP Monetary Base, AU PPI, SZ CPI, US Nfp/ Unemploy. Rate/ Factory Orders/ Durable Goods

Sources – Various news outlets including Bloomberg, Reuters, Financial Times, FactSet, Associated Press

Disclaimer: The law allows us to give general advice or recommendations on the buying or selling of any investment product by various means (including the publication and dissemination to you, to other persons or to members of the public, of research papers and analytical reports). We do this strictly on the understanding that:

(i) All such advice or recommendations are for general information purposes only. Views and opinions contained herein are those of Bordier & Cie. Its contents may not be reproduced or redistributed. The user will be held fully liable for any unauthorised reproduction or circulation of any document herein, which may give rise to legal proceedings.

(ii) We have not taken into account your specific investment objectives, financial situation or particular needs when formulating such advice or recommendations; and

(iii) You would seek your own advice from a financial adviser regarding the specific suitability of such advice or recommendations, before you make a commitment to purchase or invest in any investment product. All information contained herein does not constitute any investment recommendation or legal or tax advice and is provided for information purposes only.

In line with the above, whenever we provide you with resources or materials or give you access to our resources or materials, then unless we say so explicitly, you must note that we are doing this for the sole purpose of enabling you to make your own investment decisions and for which you have the sole responsibility.

© 2020 Bordier Group and/or its affiliates.