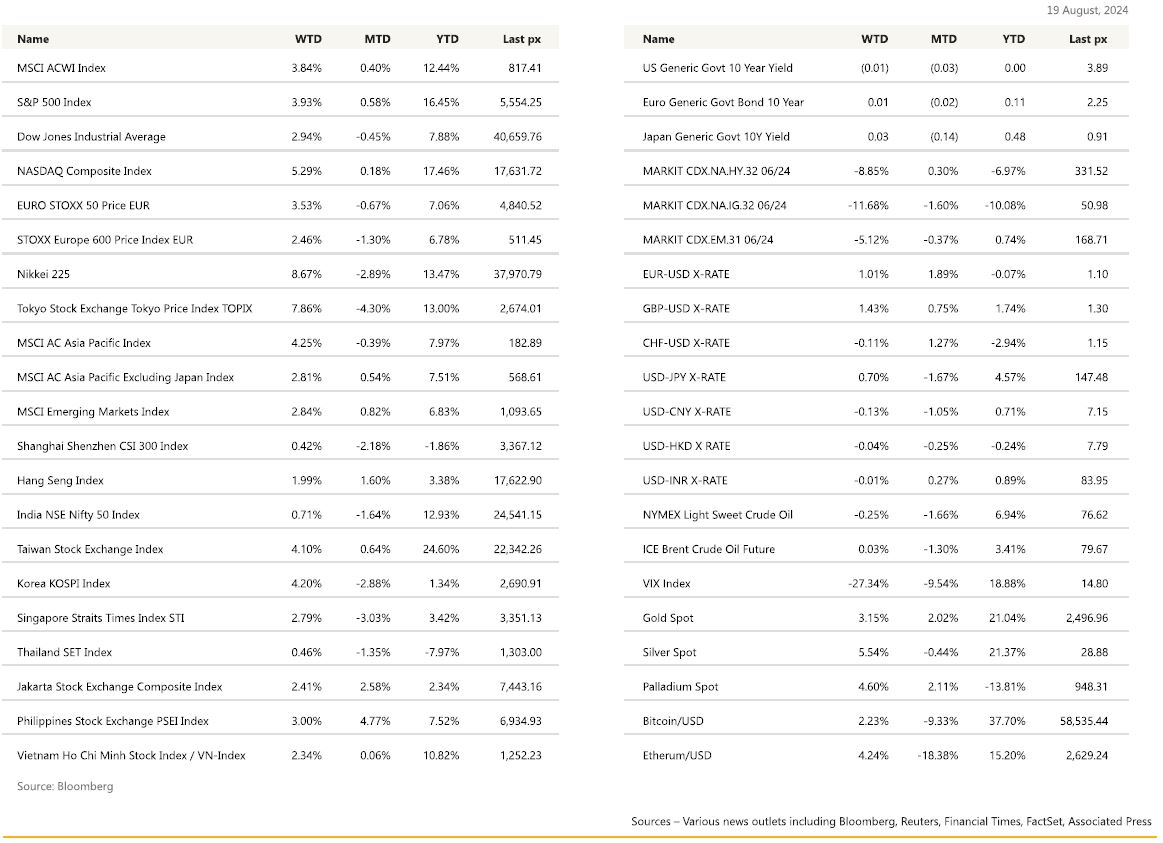

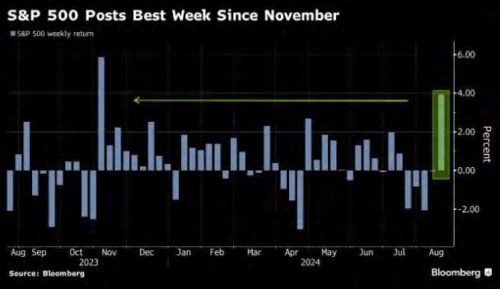

In a case of reverting to logical conclusions, good news is starting to equate to positive moves in the markets! US stocks posted its best week of 2024 after a big dead-weight, in dimming outlook for the US consumer was lifted following a better-than-expected Retail Sales data, as it showed a 1.0% MoM increase versus last month’s -0.2% helped ease fears of an economic slowdown. Weekly jobless claims fell by 7,000 to 227k which was lower than expected. This even prompted Goldmans to revise down its forecast for a recession next year from 25% to 20%, who cited these data as looking reasonably good, and possibly even a further downgrade to 15% if the economy continues its merry way. Such is the sentiment that the S&P 500 and the Nasdaq Composite both closed an admirable 4% and 5.4% respectively for the week. Cooler inflation earlier in the week also played a large part in the rally after the core reading in CPI came in as expected at 0.2% month-on-month whilst the headline year-on-year CPI reading fell to 2.9% from 3.0% previously. Core at 3.20% YoY, in line with consensus. In the details, however, worrying signs with a bounce in primary and OER rents. Shelter inflation is a focus for the FED; the bounce here increases uncertainty about the pace of the inflationary downtrend. Not enough to unwind a September rate cut, but pushes against a 50bp reduction. July Retails Sales printed higher than expected. Retail sales control group came out at +0.30% Vs +0.10% expected. The July industrial production report showed some underlying strength despite a 0.60% decline in the headline IP. Hurricane Beryl exacted a 0.30% drag on manufacturing output according to the Fed, Yet, manufacturing ex autos, still rose 0.30% in July.

Consumer sentiment rose to 67.8 for the first time in 5 months, the U. of Mich. Data showed with its inflation expectations unchanged. The Goldilocks narrative is back – slowing inflation, employment, and growth resilience and in the background, a Fed Reserve that’s about to cut interest rates.

The price action in Indices is starting to support the view that the grand rotation which saw the smaller cap outperform Mega-Tech, may be over (or close to) as both indices are starting to move in tandem.

The Fed’s engineering of a soft-landing seems to be in play.

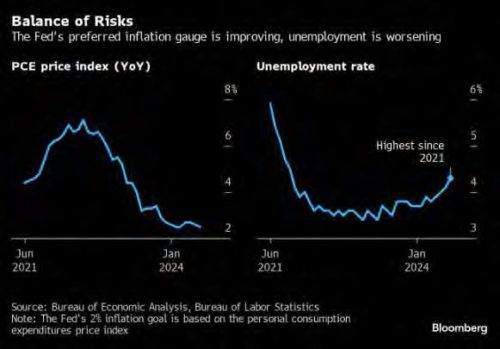

Producer prices earlier in the week went the same way as the CPI, coming in lower than expected, solidifying expectations that the Fed will start easing policy in September to keep an overly restrictive stance from stalling the economy. 25 bps is all but baked in. We’ll get more of that from Chair Powell out of the Jackson Hole symposium this week. Fed officials have reinforced the view that the central bank is prepared to cut rates. St. Louis Fed president Alberto Musalem said Thursday the time for rate cuts is nearing, echoing similar comments by Atlanta Fed president Raphael Bostic, who told the Financial Times he was open to a September rate cut, and Chicago Fed president Austan Goolsbee on the labor market and inflation.

Data this week will be light with only the last FOMC minutes and jobless claims to be of note. Jackson hole retreat will commence Friday and into the weekend. The Democratic National Convention (DNC) will be happening in Chicago, starting today till 22nd of August. In terms of macroeconomic data in the US, the latest FOMC meeting minutes will be released on the 22nd and the August manufacturing & Services PMI also will be released on the 22nd.

Cryptos had a quieter week as well hovering between BTC$56,200 andBTC$61,750.

It may be time to re-take the small/mid-cap train again, especially given a heavy tilt of a rate cut next month irrespective of the size of the rate reduction. The Russell 2000 Index is up 5.67% ytd but off its highs last seen in July: The Heptagon-Driehaus US Small Cap Equity Fund.