The event everyone was waiting for took place Friday night, when Federal Reserve Chair Jerome Powell’s speech at the Jackson Hole symposium cemented bets that the central bank will start cutting interest rates next month. Powell made clear his intention to prevent further cooling in the labour market and acknowledged recent progress on inflation. US markets rallied with real estate taking the podium as the best finisher up 3.6% for the week. The 3 major indices ended up around 1.5% for the week whist the Russell 2000 rallied 3.6%. Powell reiterated that the “pace of rate cuts will depend on incoming data, the evolving outlook and the balance of risks”. The UST10Y yield fell 5.5 bps to 3.799% whilst the more sensitive 2Y yield fell 9 bps to 3.915%. The dollar weakened across the board. Turning to data releases during the week, initial jobless claims barely rose last week, signalling that the labour market is moderating only gradually. The fourweek moving average, which smooths out some of the volatility, fell to the lowest in a month. Sales of previously owned homes rose in July for the first time in 5 months, suggesting the housing market is poised to stabilise as mortgage rates decline. Futures markets are pricing in a high probability that the central bank’s benchmark rate will be reduced by a full percentage point over the next three meetings:

Source: Bloomberg

The last FOMC minutes indicated that several Fed officials acknowledged there was a plausible case for cutting interest rates at their July meeting before the central bank’s policy committee voted unanimously to keep them steady. “Several observed that the recent progress on inflation and increases in the unemployment rate had provided a plausible case for reducing the target range 25 basis points at this meeting or that they could have supported such a decision.” Clearly, the focus has now shifted to the Fed’s other mandate of employment, with “some participants noting the risk that a further gradual easing in labour market conditions could transition to a more serious deterioration.” Data published Wednesday by the Bureau of Labor Statistics, the US Preliminary Benchmark Revisions showed payroll growth in the year through March was likely overstated by 818,000, underscoring the notion that the labour market has been cooling more and for longer than previously thought. The minutes offered little guidance on any changes to the continued wind-down of the central bank’s balance sheet, noting only that officials “judged that it was appropriate to continue the process of reducing the Federal Reserve’s securities holdings.” Fed-speak from earlier in the week echoed the sentiment with Minneapolis’ Kashkari suggesting he’s open to lowering rates in September and SF’s Daly saying that she has “more confidence” that inflation is under control. It should be noted that there are still 3 more inflation reports and 1 more employment due before the next FOMC announcement on September the 18th. Manufacturing activity improved from last month.

This week will see durable goods orders, consumer confidence, personal income & spending, and the Fed’s preferred inflation gauge, PCE at the end of the week. Headline YoY PCE is expected to pick up to 2.6% from 2.5% previously and core MoM to come in unchanged at 0.2%.

Unsurprisingly, with the weaker $, gold rallied as did cryptos with BTC at $63k and ETH at $2,750.

We continue to favour mid-capped stocks in utilities (electricity generation) and would add Cadence Design Systems, a leader in electronic system design, building upon more than 35 years of computational software expertise. Cadence’s design realization solutions are used to design and develop complex chips and electronic systems, including semiconductors.

Asian markets closed last week positive, with MSCI Asia ex Japan up 1.4%, taking YTD gains to 8.68%. Thailand was the best performer last week, up close to 4%.

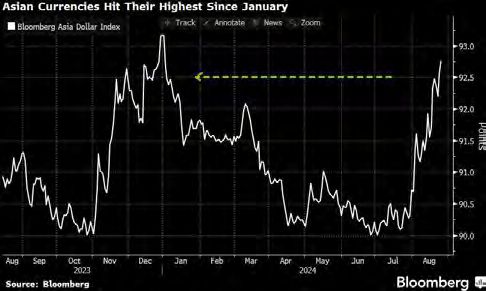

The highlight last week was Powell who confirmed that we will shortly be entering an easing cycle and that the fight against inflation is done. The Bloomberg Asia Dollar Index kicked off the week by advancing to its highest since January. The Korean Won climbed, while Singapore’s Dollar advanced to its strongest in almost a decade as traders weighed the difference between the local monetary authority’s relatively hawkish policy outlook compared with that of the Fed.

Japan data – Japan’s trade balance, which showed that export growth accelerated up to +10.3% year-on-year (vs. +11.5% expected), whilst imports were up by +16.6% (vs. +14.6% expected), which is the fastest growth for imports since January 2023. Japanese core inflation rises to 2.7% in July. Japan is ramping up promotional efforts to boost seafood exports to more destinations in Asia, the U.S., and Europe as it seeks to fill a sales gap left by a year-long Chinese import ban, the head of the Japan External Trade Organization said. China, previously the biggest market for Japanese seafood exports, banned purchases of Japanese-origin seafood citing risk of radioactive contamination.

The People’s Bank of China left the rate on its one-year policy loans, or the medium-term lending facility, at 2.3%. The one-year loan prime rate was unchanged at 3.35%, and the five-year rate remained at 3.85%. The decision underscores Beijing’s cautious approach in supporting the economy, even as China reported a rare contraction in bank loans amid weak demand. The PBOC has been walking a fine line of stimulating growth and cooling a government-bond buying spree to limit financial risks in recent months. Reflecting the lacklustre performance of the economy, the CSI 300 Index of stocks closed lower by 0.55% for the week and down 3.17% YTD.

Taiwan’s export orders rose +4.8% y/y, more than expected in July. Ministry sees August orders between +6.7% and +11.0% y/ y. Taiwan’s orders in July for telecommunication products increased 11.0% from the prior year, while electronic products rose 2.2% from a year earlier.

The consumer price index — Malaysia’s main gauge of inflation rose 2.0% in July from a year earlier, the Department of Statistics Malaysia said in a statement.

Asian central banks – The Bank of Korea kept its key interest rate at 3.50% on Thursday. The BOK also downgraded forecasts for both growth and inflation this year opening up an October cut possibility. Bank Indonesia (BI) kept its 7D repo rate unchanged at 6.25% as expected Wednesday and has lined up cuts in the fourth quarter. Bank of Thailand kept policy rate at 2.5%, also as widely expected despite pressure from new government officials to trim rates as economic growth remains tepid; bank still concerned with high household debt.