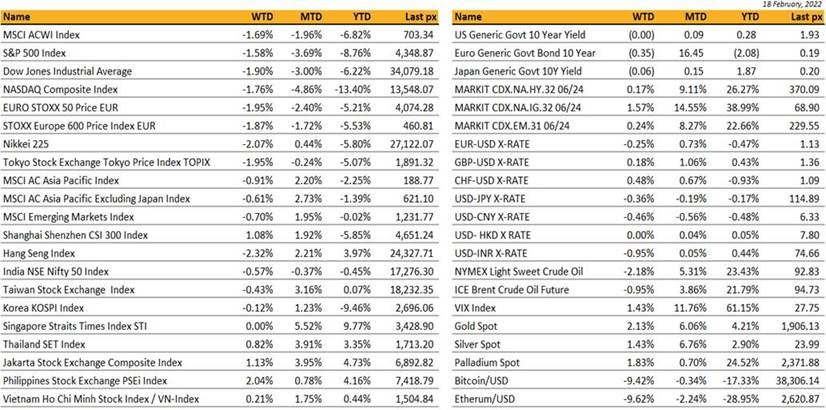

Key market moves

Source: Bloomberg

Macro Overview

Americas:

US markets ended the week lower just under 2%, marked by whip-sawing Russian-Ukraine tensions. Conflicting reports of a Russian reduction of forces at the border with Ukraine versus NATO authorities saying otherwise saw futures in the green before turning red as physical markets opened. The US has repeatedly warned of an imminent invasion by Russia.

Some relief can however, be taken after an agreement to meet was made for next week between Russian Foreign Minister Sergei Lavrov and US Secretary of State Antony Blinken in Europe.

Markets remain on tenterhooks following speeches from Fed members: Chicago President Evans called for a substantial adjustment to the current stance of monetary policy, NY President Williams said it was appropriate to increase the target rate in March and expects balance sheet reduction to start later this year, whilst Brainard said she believes it will be appropriate to commence that runoff in the next few meetings. St Louis President Bullard who had been fueling some volatility in the market favored raising interest rates by 100 bps by July the 1st, (naturally!) also said he doesn’t see much of a risk of a recession from normalizing rates, and favors beginning the balance sheet runoff in Q2.

Minutes of the last FOMC showed that the Fed was watching the situation in Ukraine and its possible impact on inflation noting that the risk of geopolitical turmoil could cause increases in global energy prices or exacerbate global supply shortages.

Economic data released during the week were mixed with retail sales beating expectations at 3.8% (vs 2%) but jobless claims rose, housing starts were lower than expected and the Philadelphia Fed Business Outlook Index came in below forecasts.

PPI was higher than expected as producers struggle with supply-chain and labor constraints.

Until we see physically what the Fed does in March, market direction or lack of, will be determined by tensions in Russia/Ukraine and inflation. This week will see the key release of PCE Deflator Price Index, which the Fed uses for its inflation target, expected to hit 6%.

Gold finally played its part and breached $1900 for the first time since June of last year as buyers returned to hedge against geopolitical risks. UST10Y yield fell to 1.928%. Cryptos, due to its correlation to risk assets were lower for the week.

Europe / Middle East (EMEA):

European markets ended lower again this week, with the Euro STOXX 600 down 1.87%. Russia-Ukraine tensions were the main talking point. In terms of sectors, banks gave back a significant portion of their year-to-date gains amid a combination of rate volatility, exposure to Ukraine and mixed updates. Travel and leisure was also a big underperformer due to Ukraine.

The possibility of a meeting between the Russian and US presidents follows days of rising fears that Moscow will launch a full invasion of Ukraine. These concerns were heightened over the weekend as Belarus said that the 30,000 Russian troops participating in joint drills would stay in the country indefinitely. Moscow has massed as many as 190,000 troops on Ukraine’s borders, despite previously pledging they would return to base. Finding an agreement will not be a simple task. Russia wants guarantees that Ukraine will never join NATO, that NATO missiles will not be deployed near Russia’s borders, and that NATO will pull all forces out of Eastern Europe. Moscow is saying European leaders are not willing to uphold the 1997 agreements, nor are they willing to fully implement the Minsk II Agreements.

Russia-Ukraine tensions was supportive for Eurozone bond markets, which saw the German Bund end the week at 0.19%, down 9 bps. However, the medium-term outlook for bonds appears to be negative as central banks are pushing towards policy normalization. Interest rates will likely need to rise this year due to a stronger inflation outlook and a consensus is emerging to end QE in September and that makes December as the most likely month for rate liftoff.

UK inflation accelerated to a 30-year high of 5.5% in January, higher than the 5.4% consensus, but it did not move BoE rate hike expectations. The market is currently pricing in as many as six rate hikes this year and considers peak inflation in the region of 7.25% in the second quarter. Thereafter, base effects should turn more favorable.

UK retail sales were much better than forecast in January, up 1.9% m/m compared with a prior 4% drop. Easing in Covid restrictions seems to be the main driver. Overall, sales volumes were 3.6% above pre-Covid levels and the proportion of online sales fell to 25.3%, the lowest since March 2020, suggesting shift to more normal spending habits. In terms of outlook however, BoE is anticipating slower consumption growth as households cut back on spending due to material downward pressure on real incomes.

Latest European car sales data showed the seventh consecutive decline because of supply shortages continuing to undermine activity. January saw a 2.4% drop in new registrations in Europe versus a year ago, which is the industry’s most prolonged stretch of weakness since the early 1990s. Despite the ongoing semiconductor shortage, the outlook for car sales remains optimistic this year, with consultant LMC Automotive seeing an 8.3% increase in sales in Western Europe this year.

Asia:

Banks in several Chinese cities have cut mortgage down payments for some homebuyers, in a move that may boost flagging housing demand. Bank of China Ltd., Agricultural Bank of China Ltd., Industrial & Commercial Bank of China Ltd. and China Construction Bank Corp. lowered the down payment ratio for first-time homebuyers to 20% from 30%.

Japan’s Gross domestic product expanded at a slightly slower-than- expected annualized pace of 5.4% in the three months through December compared with the previous quarter, the Cabinet Office reported. Economists had estimated growth of 6%. Last quarter’s growth was supposed to be the start of a more durable rebound for Japan, which has been the slowest among advanced economies to recover from the pandemic. Private consumption jumped an annualized 11.2% from the previous quarter Capital spending rose 1.6%Government spending fell 1.3%Net exports added 0.2 percentage point to non-annualized growth

Indonesia Jan trade balance reported above estimates. Trade balance surplus in January 2022 was recorded at 930 million U.S. dollars, with an export value of 19.16 billion dollars and imports valued at 18.23 billion dollars, the Statistics Indonesia (BPS) has said. Trade with the United States, the Philippines and India contributed the most to the surplus.

The Thai cabinet agreed to cut the levy by 3 baht ($0.09) per liter until May 20. The move is aimed at easing the burden on Thailand’s state- run oil fund, which has run out of cash to subsidize retail fuel sales after the recent run-up in crude prices. The move may also placate the nation’s truckers, who have been threatening a nationwide strike demanding urgent steps to rein in prices. Consumer prices rose 3.23% in January, the fastest pace since last April and above the central bank’s 1%-3% target range, issued in December.

On the virus front – Singapore will be able to ease virus restrictions more once the current omicron wave has peaked and starts to subside, health minister Ong Ye Kung said Monday in a response to questions in parliament. Hospital bed numbers are probably the biggest constraint now, he said, adding that the healthcare system is able to handle the current wave. Japan’s government will ease requirements for business travelers to the country, no longer requiring them to submit a detailed itinerary of their trip prior to arrival, the Nikkei reported. Indonesia is considering lifting all quarantine requirements for inbound travelers in April, as Covid-19 hospitalizations and fatality rates remain under control despite a resurgence in cases. Hong Kong’s hospitals are swamped. The city has commandeered thousands of hotel rooms and apartments for covid isolation wards, while children have reportedly been turned away due to a lack of beds. China’s president Xi Jinping has told Hong Kong to “take all necessary steps” to contain the city’s biggest coronavirus wave in a rare directive.

COMPANIES

Meituan shares sank as much as 18% after China issued new guidelines asking food delivery platforms to cut fees for restaurants to reduce business costs. Online food delivery platforms were also told to give preferential fees to restaurants in regions hit by the pandemic.

Singapore-based Sea Ltd. shares drop as much as 20% Monday, their biggest intraday decline on record, after India banned 54 apps it says are of Chinese origin, including the e-commerce and gaming platform’s marquee game Free Fire. While some analysts still maintain OW on the stock, the worry is for growth of Shopee India as it might be impacted if it was supported by the cash flows of Free Fire India. The India market contributes to about 3%-6% of fiscal year 2021 Ebitda of Sea’s gaming business with estimated rising proportion going ahead.

Walt Disney has chosen Mike White from its Disney Media and Entertainment Distribution group as senior VP of Next Generation Storytelling and Consumer Experiences. The company had hinted in November that Disney would be making moves into the metaverse by shifting its storytelling into a combined physical/digital world.

Gaming company Roblox shares fell more than 11% in after-hours trading Tuesday after missing fourth-quarter expectations on both the top and bottom lines. Roblox makes an open gaming platform, which lets players create their own “worlds” where they can interact and play with others over the internet and was the first major company working on the metaverse to go public. It reported revenue $770 million vs. $772 million expected, per Refinitiv consensus estimates and loss per share of 25 cents vs. 13 cents expected, per Refinitiv estimates.

US-based semiconductor developer Advanced Micro Devices finalized its purchase of Xilinx, also a US technology firm, for an estimated $50 billion.

Virgin Galactic Holdings Inc. shares are traded higher on Tuesday after the space travel company announce it will open ticket sales to the general public for the purchase of one of Virgin Galactic’s initial spaceflight reservations. During spaceflight, astronauts will experience a 90-minute journey including a signature air launch and Mach-3 boost to space. And reservations are $150,000 deposit, the total cost per 90min ride will be $450,000.

FX/ COMMODITIES

DXY. DXY USD index closed the week at 96.043 (-0.04%) last week, as safe haven currencies such as JPY, CHF and USD outperformed while geopolitical tensions relating to Russia-Ukraine remained strained. USDJPY and USDCHF were down 0.36% and 0.48% as risk off prevails. Jan FOMC minutes were fairly benign in the sense that they did not carry material signals about next steps for monetary policy. Markets now price an implied 150bp of policy tightening or six 25bp rate hikes in 2022. Data wise, US PPI, retail sales and industrial production all came in above expectations. Trading range between 94.0 and 97.5 for DXY remain intact.

GBP. GBP rose 0.18% and 0.44% against USD and EUR, as money markets now price 37bp of hikes for the March MPC meeting. UK Inflation surprised to the upside again in January, with headline rising to 5.5% yoy (consensus at 5.4%) and core also ticking higher to 4.4% yoy (consensus at 4.3%). Retail sales beats expectation as well. Better than expected UK data supported GBP.

AUD. In Australia, the December Labour Market print was a touch stronger than expectations at +13k (consensus at 0k). A modest increase in participation, to 66.2%, kept the unemployment rate flat at 4.2%. AUD rose 0.56% against USD, but fell 0.15% against NZD.

CNH. In China, the PBoC net withdrew CNY 10bn of liquidity through OMO. January CPI and PPI both came in lower than market expectations. USDCNH fell 0.64% to close the week at 6.3268 with strong support level at 6.32, and the next key support at 6.30.

Oil. WTI and Brent fell 2.18% and 0.95% as prospects of additional supply from Iran outweigh the possibility of a supply disruption.

ECONOMIC INDICATORS

M – AU/JP/EU/UK MFG/SVC/COMPS PMI Feb Prelim, CH Prime Rate

T – US MFG/SVC/COMPS PMI Feb Prelim / Cons. Confid./Richmond Fed MFG

W – AU Wage Price Index, NZ RBNZ OCR, EU CPI, US Mortg. App.

Th – NZ Trade Balance, US Initial Jobless Claims/GDP/Core PCE/New Home Sales

F – JP CPI, EU Econ./Indust./Cons Confid., US Personal Income/Durable Goods Orders/Personal Spending/Mich Sentiment