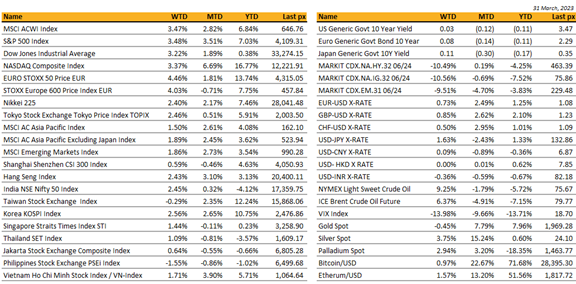

Q1 2023 ended on a positive note for Asia. MSCI Asia Pacific index was up 4% in Q1. Taiwan led the gains, up some 12% for the quarter. Followed closely by South Korea, up 10.75% for Q1. India was the worst performer in the region, down 4% since the start of the year.

Hong Kong’s market this week was supported by internet giants, as both Alibaba and JD.com announced listing plans for its units. HSI closed the week higher at +2.43%. Alibaba said it was planning to split into six units and explore fundraising or listings for most of them, the biggest corporate restructuring in its 24-year history. The six units are Cloud Intelligence, Taobao Tmall Commerce, Local Services, Cainiao Smart Logistics, Global Digital Commerce and Digital Media & Entertainment. Alibaba shares surged some 17% last week.

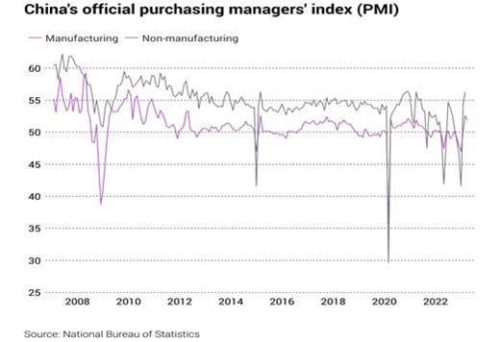

Many believe China’s economic recovery is on track coupled with government’s pledge to support private sector and foreign businesses. In his first public address to international audience as China’s premier, Li Qiang said China had acted “responsibly” in its role as a big country and offered “an anchor” for global peace. Li also struck an optimistic tone about China’s economy recovery, saying March will likely fare better than first two months of the year, citing stronger consumption, investment and sentiment. Reiterated China to purse stability, expand domestic demand, keep opening up and safeguard financial stability. Official PMIs beat expectations again with non-manufacturing reading at 58.2, the highest level since May 2011. The official composite PMI, which includes both manufacturing and services activity, rose to 57 in March, up from 56.4 in February.

Bank of Thailand raised its base interest rate by 25 bps to 1.75%, as expected, trimmed growth expectations.

Thailand has brought forward its carbon neutrality and net-zero emission target to 2050 and 2065 respectively, with environment minister Varawut Silpa-archa saying the first step in Thailand’s new adjusted timeline for net-zero is to shift the target of reducing GHG emissions from 30% to 40% within 2030. In light of this, STACS and TGO said they will work closely together to exchange ESG data and digital technology with the aim of accelerating the carbon market development in Thailand and ASEAN.

China and Brazil have reached an agreement to settle trade in renminbi. Banco BOCOM BBM, a Rio-based subsidiary of China’s state-owned Bank of Communications, will be connected to China’s Cross-border Interbank Payment System (CIPS) to facilitate trade settlements between the two nations. This arrangement marks Banco BOCOM BBM as South America’s first direct participant in the CIPS and follows the previous agreement between China and Brazil to settle trade in their own currencies.