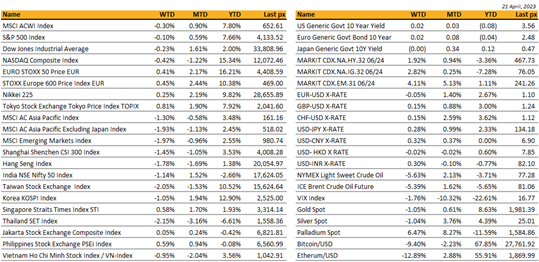

Asian markets closed lower last week. MSCI Asia Ex Japan was lower by nearly 2%.Year to date, Asian markets are holding on to their gains still with the exception of India and Thailand, both negative for the year at -2.6% and -6.6% respectively. Taiwan and South Korea markets are leading year to date gains up 10.5% and 12.9% respectively.

Last week, China reported a Q1 GDP beat. The YoY figure came in at 4.5% (vs 4.0% median estimate on Bloomberg), and was supported by strong retail sales growth in a sign of a more consumer-led post-covid recovery. However, we also saw soft industrial production (YoY 3.9% vs 4.4% expected) and fixed asset investment data for March, in contrast to a retail sales beat (10.6% vs 7.5%). So this has highlighted an uneven recovery at this stage. The jobless rate fell to 5.3% in March, and youth unemployment hit the second-highest mark on record, at 19.6%

Treasury Secretary Yellen called for a constructive and healthy relationship while rejecting idea of decoupling from China. The positive tone of her remarks contrasted somewhat with reports of President Biden set to sign G7-backed executive order restricting investment in parts of China’s economy.

US House Committee on China war gamed Taiwan invasion scenario that demonstrated significant dangers for global economy and called for arming Taipei “to the teeth.” The war game wasn’t about planning a war, lawmakers said. It was about figuring out how to strengthen U.S. deterrence, to keep a war involving the U.S., China and Taiwan from ever starting.

Exports in Japan rose +4.3% y/y in March, down from growth of +6.5% in February mainly due to a drop in China-bound shipments. Imports outpaced exports, increasing 7.3% in the year to March. This was the smallest advance in two years. Japan’s trade deficit narrowed for the second consecutive month, contracting to 754.5 billion yen ($5.6 billion) from an upwardly revised deficit of 898.1 billion yen in February. PMI was 49.5 in April, remaining in contraction territory for a sixth consecutive month. Core CPI inflation remained steady at 3.1% y/y in March.

Russia and India have resumed free trade discussions after initial talks were delayed by Covid-19 and Russia’s invasion of Ukraine. Russia’s Deputy PM made the announcement while visiting Delhi last week. Even without a free trade agreement (FTA), India-Russia trade is flourishing. Russia’s exports to India have quadrupled since the West sanctioned Moscow last year. India now imports half its oil from Russia, up from 1% before the war.

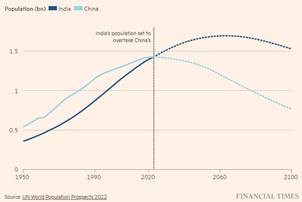

India became the world’s most populous country. With 1.4286 billion people, India now surpasses China’s 1.4257 billion; the US remains a distant third.