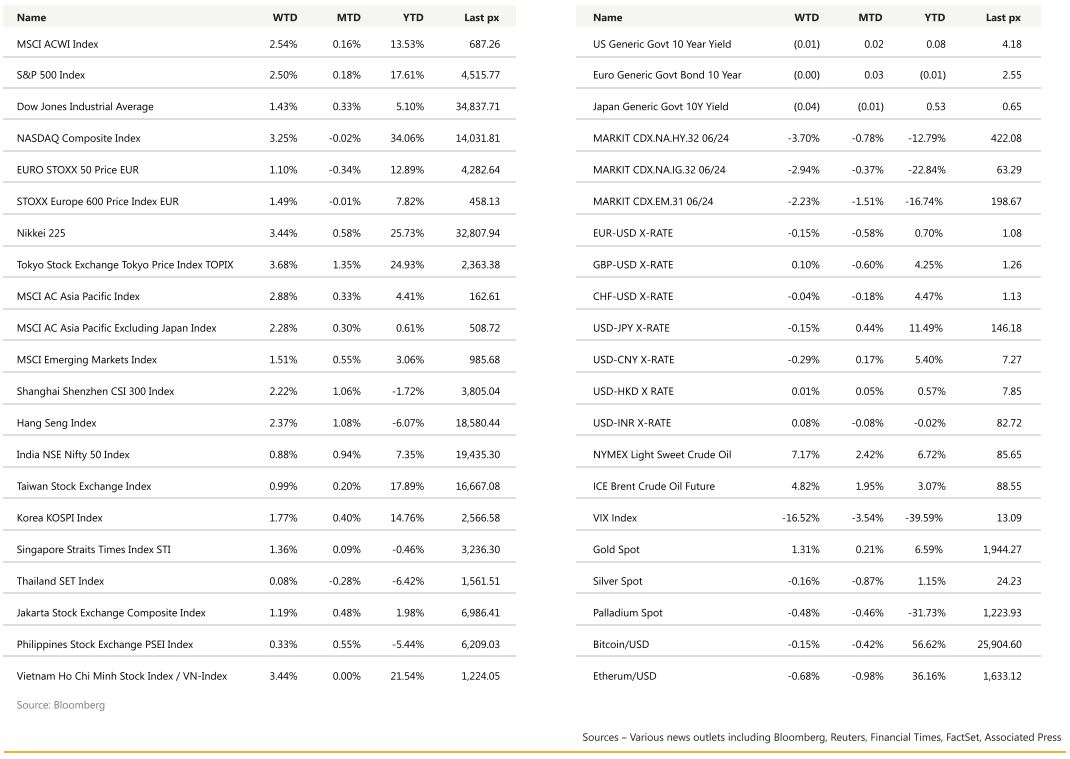

The two key data out during the week were slightly on the disinflationary side with the PCE deflator data for July at 0.2% MoM matching expectations and Friday’s US unemployment rate ticking up to 3.8%, above expectations releasing some pressure on the Fed. On a YoY basis core PCE ex-housing deflator whilst as expected at 3.3% was above June’s 3% – a level Powell flagged as being key to bringing down to the Fed’s 2% target. NFP rose by a more than expected 187k while average hourly earnings both on a MoM and YoY basis fell in July from June providing some cooling in the labour market. Earlier in the week, we also had a glimpse into the labour market with the JOLTS release showing that job openings fell in July to a more than 2-year low, extending a gradual rebalancing in the labour market. Available positions decreased to 8.83 mln from 9.17 mln in June. Both the S&P 500 and the Nasdaq posted their first down month since February though the four-day advance between Friday and Wednesday — fuelled by a deluge of economic data and subsiding expectations of a near-term recession — narrowed the loss. In focus was oil stocks which headed for its biggest weekly gains since April (WTI$85.55, Brent $88.55) driven by a slump in US inventories and ongoing speculation that OPEC+ leaders would prolong supply cuts.

Banks also recovered from the prior week’s selloff after regulators proposed new rules around long-term debt requirements for midsized banks. Analysts described the proposal — set to impact banks with more than $100 billion in assets — as being less harsh than expected and manageable for these firms.

The VIX retreated to 13.09 despite a pick-up in UST10Y yields to 4.18%. US economic activity was revised lower with GDP at 2.1% annualised in Q2 which was below the previous estimate of 2.4%. “The market is a bit bipolar; shifting from good economic news is good for earnings, to weak economic data is good for lower inflation/ Fed being done increasing,” said one analyst, and is likely to remain so until an actual pause and/or cut eventuates.

A lighter week ahead as US markets reopen Tuesday after Monday’s Labour Day holiday. ISM and factory orders among the main releases.

A higher for longer rhetoric gives us a chance to capture these higher rates which by all accounts would probably not last that long.

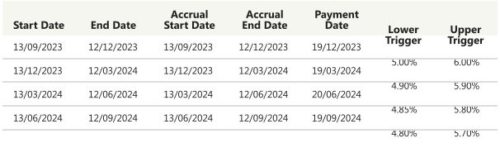

We are launching a 1-year principal protected daily range accrual note at a conditional 8% pa coupon based on the following O/N SOFR ranges (terms below):

Feel free to let us know if you’d like to participate.

Asian markets are set for a positive start. Multiple Chinese lenders are set to slash deposit rates from 1-Sep, second round of cuts in less than three months. Magnitude of reductions will be larger for longer-term deposits with 3Y and 5Y rates to be cut by 25 bp while 1Y by 10 bp and 2Y by 20 bp. Move widely expected as deposit rate adjustment took cues from 10Y sovereign bond yield and 1Y LPR.

Separately, Multiple Chinese lenders are set to slash deposit rates from 1-Sep, Magnitude of reductions will be larger for longer-term deposits with 3Y and 5Y rates to be cut by 25 bp China’s largest banks have also cut interest rates on existing mortgages of CNY38.6T ($5.3T) and deposits as latest state-directed measures to revive property sector and bolster faltering economy.

The nationwide minimum down payment will also be adjusted. It will be uniformly set at 20% for first-time buyers and 30% for second-time purchasers.

Moves are part of a targeted push by authorities to shore up consumption, drive funds to equity market and alleviate pressure on banks’ margins. China’s manufacturing activity contracted for a fifth straight month in August. The official purchasing managers’ index (PMI) rose to 49.7 from 49.3 in July, still below the 50-point level demarcating contraction from expansion.

China data heat map:

Japan‘s unemployment unexpectedly rose to 2.7%. Japan’s factory output fell more than expected in July, signalling a rocky start to the second half of the year for manufacturers as worries mount over growth in China and the global economy. Industrial output fell 2% in July from the previous month, data from the Ministry of Economy , Trade and Industry showed on Thursday. The median market forecast was for a 1.4% drop. Other data showed Japanese retail sales expanded 6.8% in July from a year earlier. Median market forecast was for a 5.4% gain.

Bank of Japan board member Toyoaki Nakamura said on Thursday it was premature to tighten monetary policy as recent increases in inflation were mostly driven by higher import costs rather than wage gains.

Indonesia is introducing a golden visa scheme to attract foreign individual and corporate investors in an attempt to boost its national economy. The five-year visa requires individual investors to set up a company worth US$2.5 million, while for the 10 years visa, a US$5 million investment is required.

Forecasts for lower rainfall in September are further threatening to disrupt supplies in cereal and oilseed crops in Asia as El Nino intensifies. While wheat output forecasts are being revised lower due to dry weather in Australia, the world’s second largest exporter, record-low monsoon rains are expected to reduce the volume of crops, including rice, in India. Insufficient rains in Southeast Asia, meanwhile, could dent supplies of palm oil, the world’s most widely used vegetable oil, while extreme weather in top corn and soybean importer China is putting food output at risk.