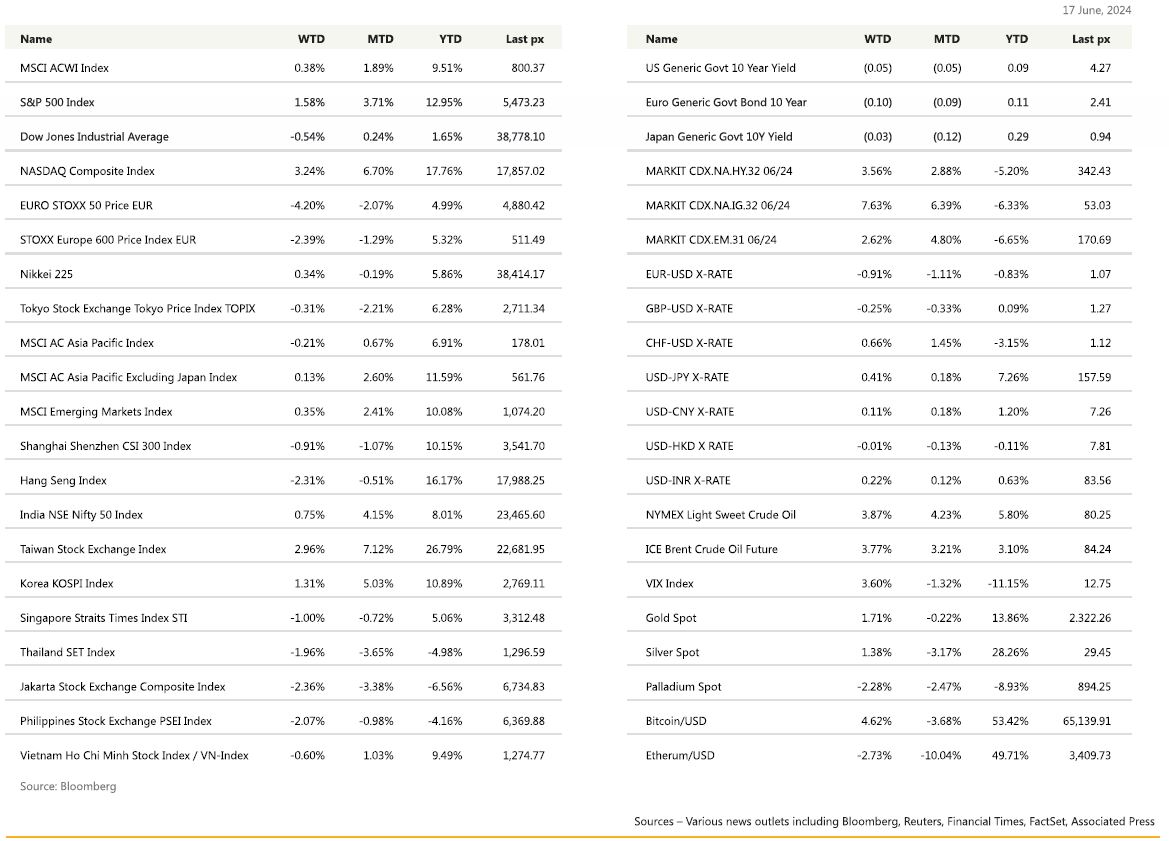

KEY MARKET MOVES

MACRO OVERVIEW

US

US stocks posted the biggest gain in four weeks even after concerns about a deteriorating US economic growth and volatility caused by political turmoil in France pushed shares lower last Friday. Recent economic data could be weighing on equities as lower-than-expected US consumer sentiment unexpectedly fell to a seven-month low after inflation reports despite coming in lower than expected, remained elevated. This comes as the latest Federal Reserve’s meeting showed that the committee is expecting only one rate cut this year.

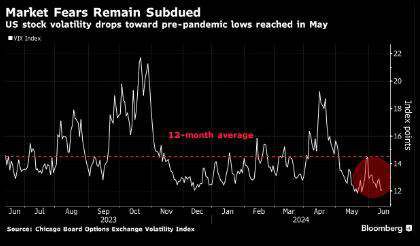

The dot plot, at Thursday’s FOMC meeting showed a median forecast on only one rate cut this year (from three in March) but four next year (up from three). While leaving the door open to an earlier cut if inflation keeps declining, the Fed appears willing to move cautiously given the uncertain inflation outlook and still, resilient economic conditions. The main drivers for market gains, expectedly, were big tech stocks. Stocks fluctuated between gains and losses during the regular trading sessions as traders assessed optimism that easing inflationary pressures will allow the Federal Reserve to cut interest rates, while also being concerned that a slowdown in growth could dampen the profit outlook. The consensus is that either ways, cuts could be on their way. The VIX remained subdued remaining below its average over the past 12 months:

Both the CPI and the PPI for May came in softer-than expected. Although the dis-inflation trend appears to have resumed, Fed policymakers stressed the need for more evidence of downward momentum before commencing their easing cycle. Core CPI month on month came in at 0.2% and headline year on year CPI was at 3.3%, both below expectations. The core consumer price index cooled to the slowest pace in some three years. PPI followed the same path, with the Final Demand YoY coming in at 2.2% versus 2.5% expected. Weekly initial and continuous claims both came in higher than expected, underpinning potentially, a slowdown in employment. The Fed’s quarterly growth and inflation projections were marginally unchanged but preliminary US consumer sentiment reading of 65.6 fell to a seven-month low. The U. of Mich. 1-year inflation forecast struck 3.3%, while the 5-10 year inflation projection ticked-up to 3.1% in June, both coming in higher than expected. A better than expected Treasury auction during the week and safe-haven buying saw UST 10s and 2’s yields dip to 4.25% and 4.70% respectively.

The new week started cautiously as optimism about corporate earnings and the premise around artificial intelligence advancing further outweighed sluggish growth in China and elevated political risks in Europe, for now. Wednesday will be a public holiday in the US in celebration of Juneteenth Day. Key data releases are light for the week, with retail sales, industrial production, and US manufacturing & services PMI’s the main prints.

It was a week for Tech behemoths – Apple with its long awaited AI features, Adobe’s sales success and Broadcom hardware which reported better than expected results powered by strong demand for AI, all of which rallied, continuing its ascend. Tesla was the odd one out, retreating despite Elon Musk re-ratifying his pay package and moving the electric carmaker’s legal home to Texas from Delaware passing by “wide margins.” Still, the underlying current supporting the sector tells us that we have not seen the top just yet.

Europe

The European Stoxx 600 index closed down 0.95% on Friday, down more than 2% on the week.

Last week, Euro area IP was broadly stable in April at -0.1% m/m after having increased 0.5% in March. Similarly, Manufacturing rose 0.1% m/m in March and falling 0.4% m/m in April. This leaves April levels of total IP and manufacturing output 1.1% and 2.2% annualized above 1Q24 respectively. Having signalled a June cut much more clearly and much earlier than it needed to, commentary from Governing Council members since last week’s meeting have been much more cautious. The bias is to cut again, but there is less conviction about the timing.

The European Parliament elections delivered a nuanced set of results. In terms of the overall seat distribution, support for centrist parties did not decline much, with mainly the Liberals and Greens losing support. This still puts current European Commission president Ursula in pole position to secure a second term and discussions were already in train to build sufficient support around her candidacy. Interest was focused on national implications, especially France, where President Macron surprisingly calling for a snap election for 30 June and 7 July, given a large swing to the far-right National Rally. The outcome remains uncertain, but there is a significant risk of cohabitation, which would see President Macron face a government led by Marine Le Pen’s NR. This would restrict Macron to the areas of external affairs, defense and justice. Since the announcement, political parties on the left have already agreed to form a coalition (New popular Front) and present single candidacies, with Melechon’s far-left La France insoumise (LFI) obtaining the highest number of constituencies.

This week we will see consumer confidence report and we expect that it will continue to nudge higher given the recent details which have shown slow but steady improvement across a range of indicators. Inflation perceptions have also improved further, which could aid the consumers’ views about their incomes. The final May HICP will be important to monitor where the flash release showed that the core inflation rose in May with services prices print sticky on the month. We expect to see a gradual improvement in sentiment in the PMIs data releasing on Friday.

Over in the UK, the REC/KPMG Reports on jobs showed an easing labour market with the permanent salaries index falling from 55.9 in April to 55.5 in May and the gap between staff availability and vacancies widening, implying a great extent of slack. The unemployment rate in UK also rose 0.1pp in April to 4.4%, and the number of vacancies fell again in the 3 months to May, for the twenty-third consecutive month.

GDP data for April showed a flat month following March’s strong 0.4% m/m. Consumer facing services were notably weak, contracting by 0.7% m/m, although services basket more than offset this with the services sector expanding 0.2% m/m.

This week, further data on flash PMIs for June and retail sales for May will be released which should shed some light on the progression in Q2.

Asia

The easing US inflation data left performance across Asia rather muted. MSCI Asia ex Japan was flat, +0.13%. MSCI Asia Pacific index was flat to, +0.21%. Hang Seng disappointed, lower by 2.3% last week. North Asia including Taiwan and South Korea were best performers, up 2.96% and 1.31% respectively.

China’s consumer price index (CPI) rose 0.3% in May from a year earlier, matching a gain in April, data from the National Bureau of Statistics (NBS) showed on Wednesday. CPI edged down 0.1% from the month before, against a 0.1% rise in April. China’s retail sales beat expectations in May, climbing 3.7% compared with a year ago, beating expectations. However, industrial output grew by 5.6% year-on-year, compared to the 6% increase expected, while fixed asset investment rose 4% compared to last May, just missing the 4.2% forecast. The People’s Bank of China held its medium term lending facility rate unchanged at 2.5%.

Japan’s wholesale inflation jumped in May, wholesale prices rise 2.4% yr/yr vs forecast +2.0%. The data complicates the Bank of Japan’s decision on how soon to raise interest rates, as price rises driven by cost pressures could cool consumption and dampen the chances of achieving the kind of demand-driven inflation it wants to see before further phasing out stimulus, analysts say.

The Bank of Japan said it would begin to “significantly” scale back its ¥6tn ($38bn) monthly bond-buying programme, a critical milestone in unwinding its ultra-loose monetary policy and tapering its expanded balance sheet. The BoJ also said it would maintain its overnight interest rate within a range of about zero to 0.1 per cent, a widely expected move.

Narendra Modi largely reappointed senior ministers from previous administration, sending signal of policy continuity and ease concerns over direction of new government. Nirmala Sitharaman retained finance ministry in strongest continuity signal, which will give investors comfort. In other appointments, Amit Shah retained home affairs, Rajnath Singh defense minister, S Jaishankar keeps external affairs portfolio. Seven other ministers kept old positions, BJP president JP Nadda to take health and family welfare portfolio

Other data from Asia:

Japan machine tool orders bounced back in May; Japan share buybacks remained a key market tailwind with activity surging in H1 this year. South Korea exports for the first ten days shrank on fewer workdays; the same report showed the US may overtake China as the country’s biggest export destination for the first time in 22 years this month if the trend continues. Taiwan’s central bank kept its policy interest rate unchanged at 2% last week. The Bank of Thailand (BoT)’s MPC voted in a 6-1 split decision to hold the policy rate at 2.50%, in line with consensus expectations.

Other data from Asia:

RBI left rates unchanged and retained its hawkish “withdrawal of accommodation” stance, setting to one side PM Modi’s narrowerthan- expected general election win. Thai inflation was 1.5% yoy in May 24, higher than estimates. Economists expect Bank of Thailand will keep rates unchanged at 2.50% next week as inflation is likely to trend higher again in 2H24F. South Korea’s consumer inflation slowed for a second straight month in May data showed. The consumer price index (CPI) in May stood 2.7% higher than a year earlier and rose 0.1% on a monthly basis. The BOK, which held interest rates steady for an 11th straight meeting in May, is expected to lower its policy rate by 50 basis points to 3.0% in the fourth quarter of 2024, according to a Reuters poll in May.

GeoPolitics

Israel – Palestine – Iran: Israel steps up strike on Hezbollah-linked targets as world looks to possible Iranian retaliation

US – Russia: New U.S. sanctions against Russia have forced an immediate suspension of trading in dollars and euros on its leading financial marketplace, the Moscow Exchange. The sanctions are aimed at cutting the flow of money and goods to sustain Russia’s war in Ukraine. Russia’s central bank has been bracing for such sanctions for around two years. Forbes Russia had reported in 2022 that the central bank was discussing a mechanism for managing the rouble-dollar exchange rate should exchange trading be halted in the event of sanctions against MOEX and its National Clearing Centre, which was also hit by the new sanctions.

The United States on Wednesday (Jun 12) dramatically broadened sanctions on Russia, including by targeting China-based companies selling semiconductors to Moscow, as part of its effort to undercut the Russian military machine waging war on Ukraine. US Treasury said it was raising “the risk of secondary sanctions for foreign financial institutions that deal with Russia’s war economy”, effectively threatening them with losing access to the US financial system. The moves are part of a broad push by the Biden administration to respond to Russia’s efforts to circumvent Western sanctions and choke off its war effort against Ukraine. U.S. officials have expressed growing frustration about China’s burgeoning trade with Russia, which they say is allowing Moscow to keep arming its military.

China – EU: The European Union threatened on Wednesday (Jun 12) to hit Chinese electric car imports with additional tariffs of up to 38% from next month following an anti-subsidy probe. The European Commission has proposed a provisional hike of tariffs on Chinese manufacturers – 17.4% for market major BYD, 20% for Geely and 38.1% for SAIC. The EU said the amount depended on the level of state subsidies received by the firms.

China has opened an anti-dumping investigation into imported pork and its by-products from the European Union, a step that appears mainly aimed at Spain, the Netherlands and Denmark, in response to curbs on its electric vehicle exports.

Credit / Treasuries

US Treasury rally led by the long-end, alongside risk-off sentiment in Europe coupled with weak economic data in the US with University of Michigan consumer sentiment falling to a seven-week low of 65.6

The US Treasury curve bull flatten with the 2years yield down 14bps, 5years down 24bps, and 10years & 30years down 22bps. US IG credit spreads widened by 3bps & US HY credit spreads end the week 10bps wider.

In term of performances, US IG gained 1.60% over the week, US HY only gained 13bps and leverage loans were down by 20bps.

FX

DXY USD Index rose 0.63% to 105.55. US Core CPI came in at 0.16% m/m (P: 0.29%) with a notable slowdown in core services ex shelter, which fell -0.04% m/m (P: 0.42%). Headline PPI fell -0.2% m/m in May (C: 0.1%; P: 0.5%) and PPI Ex Food, Energy, Trade came in at 0.0% m/m in May (C: 0.3%; P: 0.5%). Preliminary University of Michigan Consumer Sentiment survey for May showed that sentiment fell to 65.6 (P: 69.1), the lowest level in over seven months, with sentiment around both current conditions and expectations falling. On the FOMC projections, the move from three cuts in 2024 to one is explained by upward revisions to core PCE inflation forecasts, which were revised to 2.8% (P: 2.6%), 2.3% (P: 2.2%), and 2.0% (P: 2.0%) for 2024, 2025, and 2026, respectively. Growth projections were unchanged, and the unemployment rate remained at 4.0% for 2024, but was revised 10bp higher to 4.2% and 4.1% for 2025 and 2026, respectively.

EURUSD fell 0.91% to 1.0703, as risk reduction theme in Europe continues to dominate. In France, news of left-wing and right-wing coalitions forming that would effectively squeeze out President Macron’s middle drove a flight to safely. President Macron’s approval rating was down to 24%, which is its lowest level since December 2018, during the Yellow Vests protests. Apart from EUR weakening, we also have CHF strengthening due to its safe have currency demand. EURCHF fell 1.61% to 0.9529, lowest since February.

GBPUSD fell 0.25% to 1.2687. Data wise, UK GDP was flat at 0.0% m/m in April (C: -0.1%; P: 0.2%). Industrial Production fell -0.9% m/m in April (C: -0.1%; P: 0.2%), and Index of Services rose 0.2% m/m in April (C: -0.1%; P: 0.5%). Average Weekly Earnings grew 5.9% 3m/y in April (C: 5.7%; P: 5.9%) while Weekly Earnings ex Bonus grew 6.0% in April (C: 6.1%; P: 6.0%). The Unemployment Rate rose to 4.4% in April (C: 4.3%; P: 4.3%). Immediate support at 1.26/1.25.

USDJPY rose 0.41% to 157.40, as BoJ kept rates unchanged as expected, but deferred the announcement of QT plan to the July MPM. The outcome was considered dovish, as there had been some expectations that the BoJ might announce a reduction in purchases at this meeting. During the BoJ press conference, BoJ Governor Ueda says a July rate hike remains a possibility if macro conditions support it. Market implied pricing indicate a little less than a 50% probability of a July hike. Japan final 1Q24 GDP was revised to -1.8% y/y (C: -2.0%; P: -2.0%; 4Q23: 0.0%). Private non-residential investment was marginally revised up, in line with expectations.

Oil & Commodities

Oil future rose last week, with WTI and Brent crude up 3.87% and 3.77% to 78.42 and 82.62 respectively, fuelled by forecasts of strong 2024 demand from OPEC+ and the IEA. OPEC released its monthly oil market report, keeping its demand growth forecast for the year unchanged at over 2 million bpd. However, the IEA also released a new market report, but had very different projections for both demand and supply. In fact, the IEA forecast a “staggering” supply overhang of 8 million bpd in spare production capacity by 2030. The forecast angered OPEC, which called the prediction “dangerous” and warned it could inject additional volatility into oil markets.

Gold rose 1.71% to 2,333.04. Risk-off sentiment in Europe, coupled with weaker inflation data in the US signaling that the Fed may cut rates soon, supported gold prices. Key support level at 2275.

Economic News This Week

-

Monday – NZ House Sales, JP Core Machine Orders, CH Industrial Pdtn/ Retail Sales, US Empire Mfg

-

Tuesday – AU RBA OCR, EU Zew Exp./ CPI, US Retail Sales/ Indust. Pdtn

-

Wednesday – JP Trade Balance, UK CPI/ RPI, US MBA Mortg. App.

-

Thursday – NZ GDP, CH LPR, SZ SNB Policy Rate, Norway Deposit Rates, UK BoE Bank Rate, US Initial Jobless Claims/ Housing Starts, EU Cons. Confid.

-

Friday – AU/JP/EU/US Mfg/Svc/Comps PMI Jun Prelim, JP Natl CPI, UK/CA Retail Sales, US Existing Home Sales

Sources – Various news outlets including Bloomberg, Reuters, Financial Times, FactSet, Associated Press

Disclaimer: The law allows us to give general advice or recommendations on the buying or selling of any investment product by various means (including the publication and dissemination to you, to other persons or to members of the public, of research papers and analytical reports). We do this strictly on the understanding that:

(i) All such advice or recommendations are for general information purposes only. Views and opinions contained herein are those of Bordier & Cie. Its contents may not be reproduced or redistributed. The user will be held fully liable for any unauthorised reproduction or circulation of any document herein, which may give rise to legal proceedings.

(ii) We have not taken into account your specific investment objectives, financial situation or particular needs when formulating such advice or recommendations; and

(iii) You would seek your own advice from a financial adviser regarding the specific suitability of such advice or recommendations, before you make a commitment to purchase or invest in any investment product. All information contained herein does not constitute any investment recommendation or legal or tax advice and is provided for information purposes only.

In line with the above, whenever we provide you with resources or materials or give you access to our resources or materials, then unless we say so explicitly, you must note that we are doing this for the sole purpose of enabling you to make your own investment decisions and for which you have the sole responsibility.

© 2020 Bordier Group and/or its affiliates.