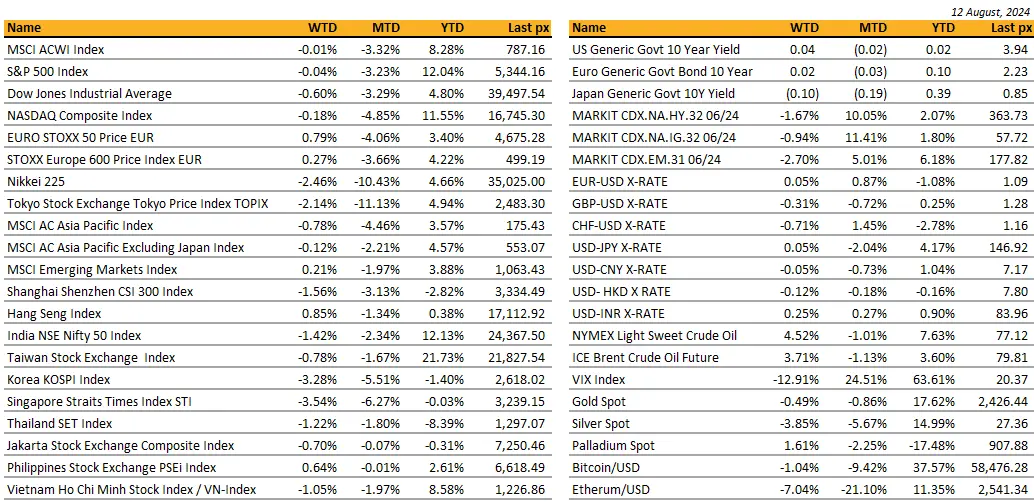

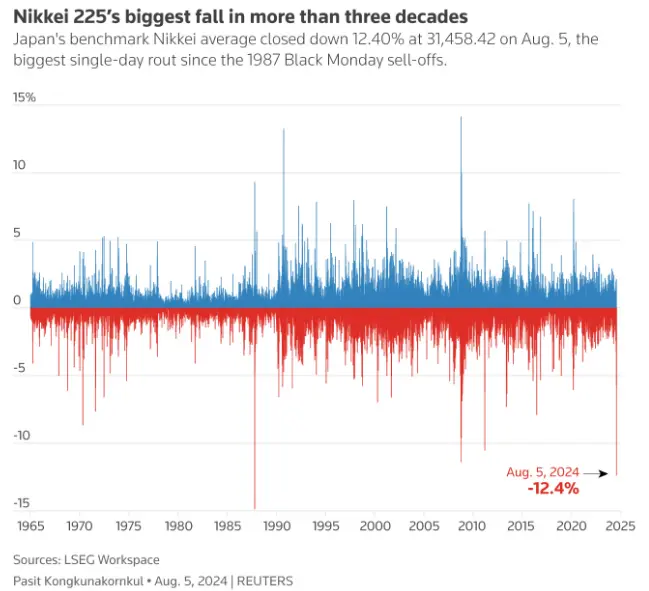

Black Monday, Turn around Tuesday, some reprieve came on Wednesday when the Bank of Japan said it won’t raise its policy interest rate if financial markets are unstable, according to deputy governor Shinichi Uchida. Recent market moves are “extremely volatile” and the central bank needs to keep monetary policy easy for the time being, Uchida said. Monday saw a ~12% sell off for the Nikkei. The single biggest one day fall since 1987. Japan saw the highest turnover day ever for TOPIX was more than 8 trillion YEN – so there was real volume backing the move. The benchmark indexes in Japan had fallen by more than 20% from their all-time highs on July 11 end of trading on Monday. Concerns about the markets were exacerbated by investors winding down yen-funded trades that had been used to finance the acquisition of stocks for years after a surprise Bank of Japan rate hike last week. The Nikkei enjoyed a decent retracement on Tuesday, as comments from the Fed’s Daly and a stronger-than-expected ISM services report soothed fears of a panic Fed cut next week. Nikkie closed the week lower by 2.46%. YTD it is still up 4.66%.

The dollar-yen pair has now fallen more than 9% as of this morning, since peaking five weeks ago and is in highly oversold territory. The yen is therefore vulnerable to any upside surprises in U.S. macro data. This could help Japanese equities stabilize further . There is little expectation of sustained momentum in the yen’s decline. CFTC data indicates that speculative short positions against the yen were rapidly unwound by the end of July. Historically, the liquidation of carry trades has often led to significant yen strengthening. For example, in 2007, net short positions in the yen were similar in size to current levels, and the unwinding process saw the yen strengthen significantly, especially during the 2008 Lehman Brothers collapse. Similarly, in 1998, yen appreciation was rapid following the LTCM crisis. Although there is no immediate financial crisis looming today, geopolitical risks and other factors are amplifying upward pressure on the yen. Mizuho Research & Technologies has estimated the fair value of USD/JPY to be around 142-143 based on current yield differentials. However, the potential narrowing of the policy rate gap between the US and Japan suggests further yen appreciation could be on the horizon, with some analysts eyeing a possible move towards the 130 level.

The RBA has just left the cash rate on hold at a 12-year high of 4.35% for a sixth meeting in a row, despite the looming prospect of high inflation becoming entrenched. In the post-meeting statement, the board kept its options open on future moves, preferring not to rule anything in or out. Meanwhile, refreshed economic forecasts from the RBA showed that underlying inflation will ease to 3.5% by the end of this year, and then hitting 3.1% in mid-2025.

The Reserve Bank of India (RBI) kept its key interest rate unchanged at 6.5% on Thursday as expected. According to the RBI governor, “Growth remains resilient, inflation has been trending downward and we have made progress in achieving price stability, but we have more distance to cover.”

China – Caixin services PMI 52.1 vs consensus 51.4 and 51.2 in prior month and the Caixin Composite PMI 51.2 vs 52.8 in prior month. China’s consumer price index (CPI), a main gauge of inflation, increased by 0.5% year on year in July. In contrast, the producer price index (PPI) saw a year-on-year decline of 0.8% in July, maintaining the same rate of decline as in the previous month. Trade data – China’s imports jumped 7.2% y/y in July, beating Reuters forecast of 3.5% and reversing 2.3% drop in prior month; while exports rose 7% and came below 9.7% consensus and 8.6% growth in June. Exports also grew for fourth straight month. Trade surplus stood at $84.65B, below $99B expected and $99.05B in June, which was at record high since at least 1990. Bloomberg added Chinese economy was heading to a bumpy start to Q3 while grappling with weak domestic demand and prolonged property market doldrums. Boom in exports was one of few bright spots this year however is increasingly inviting more tensions with EU and US.

Indonesia’s 2Q 2024 GDP came in slightly better than expected, up 5.0% q/q on a par with the pre-pandemic trend. The stronger than expected print was led mainly by domestic demand.

Last Wednesday, Investors were picky on the levels where they are willing to buy long-dated US Treasuries. The 10Years US Treasury auction tailed by 3bps with the highest primary dealer take up since April, driving the US Treasury curve another leg steeper in the process. Following this auction, and after 25Months of inversion, the 2-10 part of the curve almost got back to being normalized again, with the 2years yield only 2bp higher than the 10years yield (see chart below). The 2-10 ended the week with a 10bps inversion.

Huge volatility on interest rates early last week during what could be considered Black Monday. But volatility did not last long, and yield normalized over the remaining part of the week. The shape of the US Treasury curve did not drastically change, with the 2years & 5years yield up 19bps, the 10years yield gained 16bps and the 30years up by 12pbs. Credit spreads, after initially widening on Monday, finished the week tighter by 5bps for US IG & 29bps tighter for US HY.

In term of performances, US IG lost 55bps, US HY gained close to 1% and leverage loans gained about half a percent.