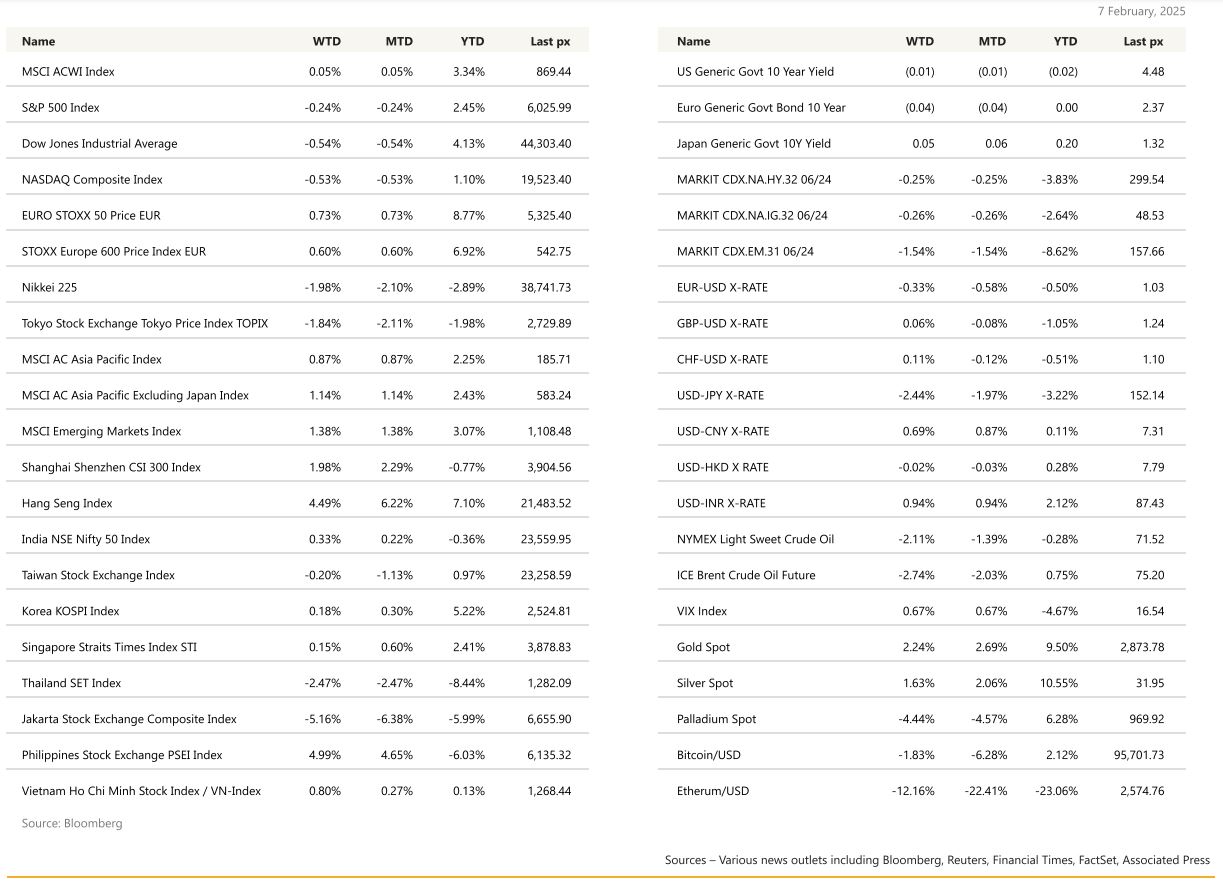

KEY MARKET MOVES

Source: Bloomberg

MACRO OVERVIEW

US

After rallying for the better half of the week, US stocks ended the week down about half a percent after President Trump on Friday, promised to unveil reciprocal tariffs next week in a major escalation of his trade war. The slide on Friday extended the S&P 500’s losses into a 2nd week. Outlooks from tech giant, Amazon missing estimates and disappointing earnings results from Alphabet Inc earlier, also contributed to the selloff. What spooked the markets on Friday was President Trump saying that his plans would affect “everyone,” without specifying exactly what measures he would take. The president said he was considering tariffs targeting automobiles, among other measures, to “equalize” trade.

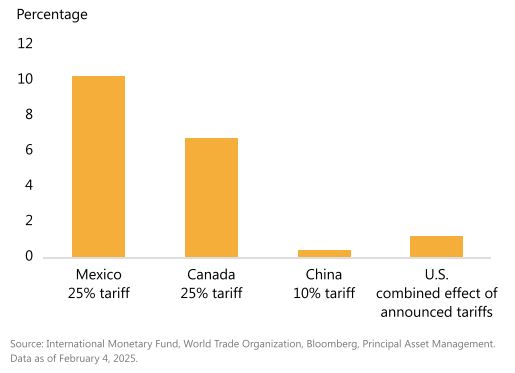

Assuming all the announced tariffs eventually advance, the estimated negative growth hit to both Mexico and Canada could range from 7% to 10% of GDP—large enough to potentially throw both into a deep recession. China could see a direct GDP drag near 0.4%—while smaller, it likely exacerbates the ongoing property market-induced downturn. Notably, U.S. growth is also likely to be impacted, by an estimated 1.2%. Such a growth shock will likely put pressure on policy measures such as tax cuts and deregulation to help cushion downside risks. Meanwhile, tariffs could result in a near-term increase in inflation, potentially pushing headline inflation back toward 4%. (Principal Asset Management Feb. 2024).

Over the weekend, President Trump said he will announce on Monday, 25% tariffs on all imports of steel & aluminium. He did not specify when the duties would take effect. He also said he would announce reciprocal tariffs later in the week on countries that tax US imports. When asked about Trump’s desire to lower interest rates, Treasury Secretary Scott Bessent said the Administration’s focus is on bringing down borrowing costs via 10-year Treasury yields, rather than the Federal Reserve’s benchmark short-term interest rate.

The U. of Mich consumer sentiment fell to a 7-month low on a spike in ST inflation expectations saw swap traders push the next back rate to September. Inflation expectation for 1-year rose to 4.3% vs expectations of 3.3%. Inflation expectations are prone to downward revisions in the final read, but the spikes here are notable: negative impact of tariff policy cited in the press release. The 5-10years inflation forecast printed at 3.30% Vs 3.20% expected, the highest in more than a decade.

We also had the US unemployment report on Friday which came in lower than expected at 143k with the unemployment rate falling to 4% from 4.1%. These numbers might look weaker, but when we include the upwards revisions of the previous Month, NFP was revised up by 51K jobs & private payrolls was revised up by 50K jobs, over two Months, these jobs indicators look reassuring. Some of the weakness in employment this month may be due to unseasonably cold weather, as well as the LA wildfires, which led to evacuation orders beginning the week before the survey reference period. There is a continued improvement in underlying trends with the 3mth average gains for headline (237k) and private payrolls (209k) solidly above their six-month averages of 178k and 145k. The January Average Hourly Earnings have surprised on the upside, MoM printed at +0.50% (Consensus +0.30%), which push the YoY at 4.10% Vs 3.80% expected. The previous month YoY was also revised up by twotenth of one percent. The labor force participation came out at 62.60% vs 62.50% expected. Overall, the job data for January are still showing a pretty resilient job market in the US.

The JOLTS job openings fell to 7.6 mln, down from November’s revised 8.156 mln. Quits rate came out at 2%, in line with previous Month, which was revised higher. Layoffs rate remains unchanged at 1.10%. January ADP Employment change printed at 183K Vs 150K expected while the previous month was revised up by 54K jobs to reach 176K. The December US Trade Balance printed at -98.4Bn, a bigger deficit than expected. This number can probably be explained by quite a significant amount of front loading before any trade tariffs could be put in place by the new US administration.

January final US Services PMI printed at 52.9, exactly in line with consensus. The ISM services index however printed lower than expected at 52.8 Vs a consensus of 54.0. It is, in a way, reassuring that these two survey indices have now converged to the same level as these two surveys are supposed to express, more or less, the same information, the main difference being the pool of people within corporate that are questioned.

Fed speak post data saw Minneapolis’ Kashkari saying the US labor market had cooled but remained solid, and interest rates are likely to decline “modestly” in 2025. Fed Governor Adriana Kugler said it’s appropriate to keep the Fed’s benchmark interest rate where it is for some time. We also had Chicago’s Goolsbee mentioning that fiscal policy uncertainty may lead to fewer rate cuts, although he still sees some reductions over the next 18 months.

This week will see CPI, PPI and retail sales among the key releases. Fed Chair Jerome Powell, will offer his semi-annual testimony to lawmakers on Tuesday and Wednesday, and is likely to highlight the resilient economy as a key reason central bankers are in no rush to further cut borrowing costs. Bloomberg expects core CPI MoM to come in at 0.3% from 0.2% and the YoY headline CPI to remain unchanged at 2.9%.

Europe

European markets finished softer, reversing some earlier strength. The Eurostoxx 600 was higher by 0.60% over the week, which was contributed by a rise in volatility in part due to the U.S – China trade spat.

In terms of the ECB, there was significant focus last week on updated estimates of the neutral policy rate from the ECB staff. This largely reaffirmed its view from last year with a range of 1.75% to 2.25%. The ECB is set to enter a new phrase of unpredictability as the terms of seven of its 26 interest ratesetters end by December, marking its biggest personnel shakeup since 2019. These are namely, Finland, Netherland, Austria, Portugal, Malta, Slovakia, and Slovenia. Balance between hawkish and dovish policymakers might shift just as the ECB has to decide how low to cut rates.

In data, the Euro area composite PMI has picked up almost 2pts, with Germany improving and its labor market data looking less acute. Euro area consumer spending also continues to grow, with weakness more concentrated in capex. Euro area headline inflation was up 0.08%-pt to 2.52%oya in January. The increase was mostly driven by energy price inflation increasing 1.71%-pts to 1.84%oya. Food price inflation declined 0.29%-pt to 2.32%oya and core inflation declined 0.02%-pt to 2.69%oya, with core goods inflation moving sideways (0.52%oya) and services inflation down 0.06%-pt to 3.91%oya.

The final Euro area PMI saw only small revisions and therefore confirmed a 1.9pt increase over the past two months, leaving the composite output index at 50.2. An upward revision in Germany (flash 50.1), which was offset by a downward revision in France (flash: 48.3). Despite the mixed country details, the Euro area PMI has gained 1.9pts since November. Euro area retail sales contracted slightly by 0.2%m/m in December, following a small downward revision for November. Production in the German manufacturing sector declined by 4.9% in 2024. This was the fifth annual decrease in the last six years. Industrial production is now 13% below the peak reached in 2018. Nevertheless, these are still only a few green shoots in a challenging economic environment for the German industry. Despite further interest rate cuts on the horizon, we rather expect a kind for “wait-and-see” attitude in the German industrial sector with regard to US trade policy and the course of the new German government. Deutsche Bank expect industrial production in Germany to decline by 1.5% in 2025 on average.

French Prime Minister Francois Bayrou forced his 2025 budget bill through the lower house of parliament, using a constitutional provision, which did trigger a vote of no-confidence in the parliament, but this time the new French Government survived it.

The BoE cut rates by 25bps to 4.5% at its February meeting. The decision was as expected, but the general messaging from the MPC about the rate path ahead was very mixed. Three groups with different opinions have formed on the committee, with views becoming more polarized. But the overall tone was more hawkish than expected, and more than is implied by the two votes for 50bp cuts. What wasn t expected was the scale of the growth downgrade in the bank s accompanying economic forecasts. The bank now predicts that the British economy will only grow by 0.75% this year, down from its previous forecast of 1.5% just three months ago. But at the same time, it now expects CPI inflation to hit a much higher peak of 3.7% in 3Q (previously 2.8%). This is a touch higher than the forecast (3.5%). The most interesting part of the BoE’s forecast was the medium term, where inflation was shown still above target two years hence (at 2.3%) based on a path of rates that only gets to 4.16% by year end. This is related to higher imported inflation, but also the lagged impact of firmer than expected wage growth this year (3.75%) as well as weaker productivity.

This week, we will see industrial production figures and the unemployment figures in the Euro Area and GDP data in the UK.

Asia

All Greater China’s main boards closed higher last week. The strongest gains were seen in Hong Kong-listed technology stocks, pushing its tech index 7% higher YTD. Hang Seng tech, still basking in Deep Seeks advancements , is up 15.27% YTD. Trade tariff rhetoric cooled between US /Canada and US/Mexico with tariffs on hold while Beijing’s response to Trump’s tariffs seen as moderate. No Trump-Xi call last week. With regards to China, Trump also said today he would maintain duty-free exemption for low-value packages from China and Hong Kong, saying the exception would remain in place until systems to process and collect tariffs are implemented.

Travel and spending during China’s Lunar New Year holiday hit new records this year. A total of 501 million trips were made, and Tourism spending surged by 7%, reaching 677 billion yuan ($93 billion). A record-breaking 187 million people went to the cinema over the holiday, lifting the box office to a record high of 9.5 billion yuan ($1.32 billion). Separately, the China Index Academy reported sales of new housing and prices for existing home units both continued to fall in January. It said the average price per square meter for existing properties fell more than 7.0% y/y in 100 of China’s top cities, and the value of property sales fell by almost 17% y/y.

Trump said last week Modi would be coming to White House, noting that during their call he pressed Modi to address trade imbalance and boost purchases of US-made military equipment (Bloomberg). India is more vulnerable to a trade fight with Trump, running $35.3B surplus with US. Trump has also accused India of being a trade abuser and last week signaled potential action against India for causing economic “harm” to US (Indian Express). However, recent actions by India being seen as attempt to placate Trump in a bid to avoid tariffs (Bloomberg). Indian budget on Saturday included cuts to import duties covering several products, including motorcycles, which follows previous Trump complaints about tariffs being levied on Harley-Davidson bikes.

The Reserve Bank of India, said that the rate-setting panel has pegged the nation’s GDP growth for FY26 at around 6.7%. This projection is marginally higher than the earlier forecast of 6.6 % announced in December 2024. The RBI expects economic growth for the quarters of the next fiscal year starting April 1 as follows: Q1 at 6.7%, Q2 at 7%, Q3 at 6.5%, and Q4 at 6.5%.

Other data points in Asia – Japan PMI shrank at quickest pace in 10 months with autos and manufacturing notably weak. South Korean manufacturing returned to modest expansion amid improvement in external demand.

GeoPolitics

US – Tariffs:

The United States will move to impose 25 per cent tariffs on steel and aluminium imports on Monday (Feb 10), President Donald Trump said over the weekend.

President Trump agreed to delay 25% tariffs against Mexico for 1 month after a conversation with Claudia Sheinbaum. Mexico will send 10,000 troops to the border to stem the flow of fentanyl and migration.

Duties on China however went into effect Tuesday, and China retaliated. China’s Finance Ministry retaliated by imposing levies of 15% for U.S. coal and LNG and 10% for crude oil, farm equipment and some autos. The new tariffs on U.S. exports will start on Feb. 10, the ministry said. China also said it was starting an anti-monopoly investigation in Alphabet Inc, while including both PVH Corp , the holding company for brands including Calvin Klein, and U.S. biotechnology company Illumina on its “unreliable entities list”.

US- Palestine – Israel: President Donald Trump pledged on Tuesday that the U.S. would take over the war-ravaged Gaza Strip after Palestinians are resettled elsewhere and develop it economically, a move that would shatter decades of U.S. policy toward the Israeli-Palestinian conflict. Five Arab foreign ministers and a senior Palestinian official sent a joint letter to US Secretary of State Marco Rubio on Monday opposing the idea of displacing Palestinians from Gaza. It was signed by Egypt, Jordan, Qatar, Saudi Arabia and the United Arab Emirates, as well as the Palestinian Authority. Saudi Arabia said it would not establish ties with Israel without the creation of a Palestinian state, contradicting President Donald Trump’s claim that Riyadh was not demanding a Palestinian homeland when he said the United States wants to take over the Gaza Strip.

US- Israel – ICC: US president placed financial sanctions and blocked visas for the ICC employees and their families, in a move that coincided with Israeli Prime Minister Benjamin Netanyahu’s visit to Washington. The order also applies to officials who investigate US citizens. The order says the court is a threat to the “sovereignty” of the US that “undermines the critical national security and foreign policy work” of the country and allies such as Israel. In November, the ICC issued arrest warrants for Netanyahu and his then-defence minister Yoav Gallant “for crimes against humanity and war crimes”. Trump also took measures against ICC officials in 2020, authorising an asset freeze and blocking their family members from coming into the US after the court began investigating alleged US actions in Afghanistan.

US – Russia- Ukraine: President Donald Trump on Monday said he wanted a deal granting the US access to Ukraine’s rare earths resources in exchange for continued military and economic aid to Kyiv as it struggles to halt Russia’s invasion. Kyiv holds vast reserves of titanium, iron ore and coal, as well as about 500,000 tonnes of untapped lithium, collectively estimated to be worth tens of trillions of dollars. Some of these resources are at risk of being lost to Russia’s advancing forces in Ukraine’s east, or have already fallen under Russian occupation.

While supportive of Trump’s enthusiasm to bring the three-year war to an end, the American leader’s suggestion that he had formulated part of a plan with Russia without Ukraine has irked leaders in Kyiv. An alleged Ukraine War truce will include ceasefire by Easter and some land transferred to Russia.

US – India: A US military plane began deporting Indian migrants, as per news agency Reuters, implementing US President Donald Trump’s hardline stance against an estimated 11 million undocumented migrants in the United States. India is the farthest destination of US military flights deporting migrants, with the Pentagon stating flights to deport over 5,000 migrants from El Paso, Texas, and San Diego, California. So far, military aircraft have flown migrants to Guatemala, Peru and Honduras. The US President had said after a call with Prime Minister Narendra Modi that the latter “will do what’s right” when it comes to taking back illegal Indian immigrants from America. India accounts for a relatively small share of illegal migration to the US, making up only 3% of unlawful crossings according to the US border protection data.

AI Race: A growing list of countries, including South Korea, Italy and France, have voiced concerns about DeepSeek’s security and data practices. Australia upped the ante mid week by banning DeepSeek from all government devices, one of the toughest moves against the Chinese chatbot yet.

US – Panama: Panama rejects Trump administration claim it agreed to allow American warships to transit canal for free.

Credit / Treasuries

The overall strong macroeconomic data in the US last week, and especially the job data last Friday, supported a rebound in short term US Treasury yield. Over the week, the 2years yield gained 2bps, 5years yield lost 3bps, 10years yield lost 6bps and the long bond lost 10bps of yield. The move on the medium to long part of the curve can probably be explained by the Treasury quarterly refunding announcement mid of last week when the US Treasury said that they plan on keeping coupon bond supply stable this year, announcement which should alleviate a major concern for prospective buyers. They said that Treasury will maintain current bond auction sizes for “at least several quarters,” a more conservative stance than what was anticipated and at odds with the TBAC’s uniform view to ease this guidance. Coupled with Bessent’s statement that this Administration will focus on 10-year Treasury yields, this suggests that future supply increases will be carefully managed and likely smaller than previously anticipated. US IG 5years credit spreads tightened over the week by 1.5bps while US HY 5years credit spreads tightened by 7.5bps. US IG gained about 30bps last week while US HY gained only about 11bps.

FX

DXY USD Index fell 0.30% to 108.04 as markets perceive the tariff situation between US and China as encouraging.

Following US tariffs of 10% on top of previous tariffs on all goods on China, China’s response was restrained in an attempt to avoid a full trade war as China did not include tariffs on American farm products, which would have suggested a significant escalation. However, over the weekend, it was reported that reciprocal tariffs would be unveiled this week in a major escalation of his trade war with US economic partners, affecting everyone. US macro data was mixed. Nonfarm payroll missed consensus (A: 143k, C: 175k), but underlying details were strong with unemployment rate below (A: 4.0%, C: 4.1%) and average hourly earnings above (A: 0.5%, C: 0.3%). UMich below consensus (A: 67.8, C: 71.8) and 1y Inflation Expectations surged higher to 4.3% (P: 3.3%), the highest reading since Nov 2023. Both US Mfg ISM and PMI above consensus, but ISM services unexpectedly fell to 52.8 (C: 54.1; P: 54.1). Trading range on DXY between 107 and 110, and a break on these levels suggest a change in trend.

European Currencies performed mixed against USD. EURUSD fell 0.33% amid a renewed focus on the potential of trade escalations with the US. On EU Macro, CPI a bit stronger with headline -0.3% (C: -0.4%) and Core +2.7% (C: 2.6%). Retail sales below consensus (A: -0.2%, C: -0.1%, P: 0.0%). GBPUSD came in flat at 1.2402. BoE cut rates by 25 bps as expected, with a vote spilt of 7-2, with 7 in favor of a 25bp cut and 2 in favor of 50bp cut (dovish messaging). However, the forecasts revision seemed hawkish, with a forecast of 1.9% terminal inflation.

USDJPY fell 2.44% to 151.41 as the market revised up Japan terminal rate pricing on the back of hawkish communication by BoJ officials and the recent strong labor/inflation data. December nominal wage growth came in higher than consensus (A: 4.8%, C: 3.7%). Hawkish comments from BOJ’s board member Tamura Naoki stating that the central bank must raise rates at least to around 1% in the latter half of fiscal 2025. Immediate support level at 151/150, while resistance level at 153/155.

AUDUSD rose 0.90% to 0.6274 driven by encouraging US-China tariffs situation. On AU Macro, Australia retail sales beat consensus (A: -0.1%, C: -0.7%).

USDCAD fell 1.71% to 1.4293 after touching a high of 1.4793 earlier in the year. On CA Macro, employment grows 76k (C: 25k) while the Unemployment Rate unexpectedly falls.

Oil & Commodity

Oil Futures fell last week, with WTI and Brent falling 2.11% and 2.74% to 71 and 74.66 respectively. OPEC+ leaves production levels unchanged despite calls from President Trump for cheaper oil prices. Immediate support on WTI and Brent at 70 and 74 respectively.

Gold rose 2.24% to close the week at 2861 (record high). USD weakness and increased uncertainty in global financial markets aids the rise in gold prices. China’s central bank expanded its gold reserves for a third month in January, signalling ongoing commitment to diversify reserves despite high prices.

Economic News This Week

- Monday – Norway CPI, EU Sentix Inv. Confid., US NY Fed 1Yr Inflation Exp.

- Tuesday – US JOLTS/ Factory Orders/ Durable Goods Orders

- Wednesday – US MBA Mortg. App./CPI/Federal Budget Balance

- Thursday – JP PPI, NY 2Yr Inflation Exp., UK Indust./Mfg Pdtn/GDP, SZ CPI, US PPI/Initial Jobless Claims

- Friday – NZ Biz Mfg PMI/Food Prices, EU GDP, CA Mfg Sales, US Retail Sales/Indust. Pdtn

Sources – Various news outlets including Bloomberg, Reuters, Financial Times, FactSet, Associated Press

Disclaimer: The law allows us to give general advice or recommendations on the buying or selling of any investment product by various means (including the publication and dissemination to you, to other persons or to members of the public, of research papers and analytical reports). We do this strictly on the understanding that:

(i) All such advice or recommendations are for general information purposes only. Views and opinions contained herein are those of Bordier & Cie. Its contents may not be reproduced or redistributed. The user will be held fully liable for any unauthorised reproduction or circulation of any document herein, which may give rise to legal proceedings.

(ii) We have not taken into account your specific investment objectives, financial situation or particular needs when formulating such advice or recommendations; and

(iii) You would seek your own advice from a financial adviser regarding the specific suitability of such advice or recommendations, before you make a commitment to purchase or invest in any investment product. All information contained herein does not constitute any investment recommendation or legal or tax advice and is provided for information purposes only.

In line with the above, whenever we provide you with resources or materials or give you access to our resources or materials, then unless we say so explicitly, you must note that we are doing this for the sole purpose of enabling you to make your own investment decisions and for which you have the sole responsibility.

© 2020 Bordier Group and/or its affiliates.